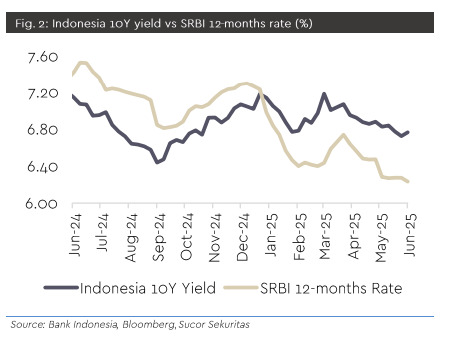

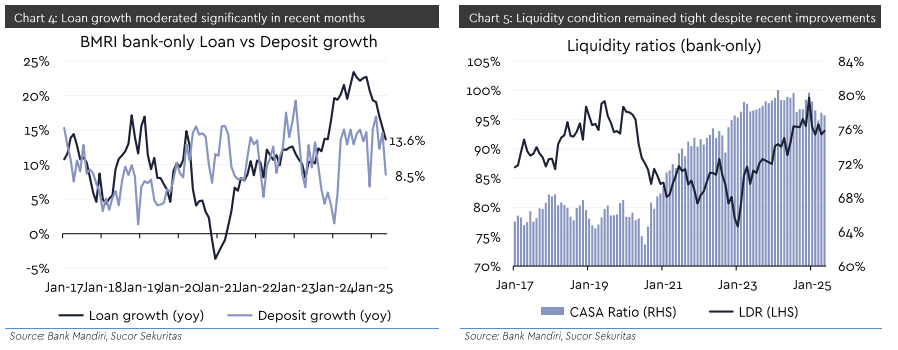

As we know, Bank Indonesia introduced SRBI to help stabilize the Rupiah and strengthen domestic currency demand. For banks, it was a balancing act. While SRBI offered attractive returns and short tenors, the mandatory participation absorbed liquidity across the sector throughout 2024, limiting the room for credit growth and putting pressure on margins.

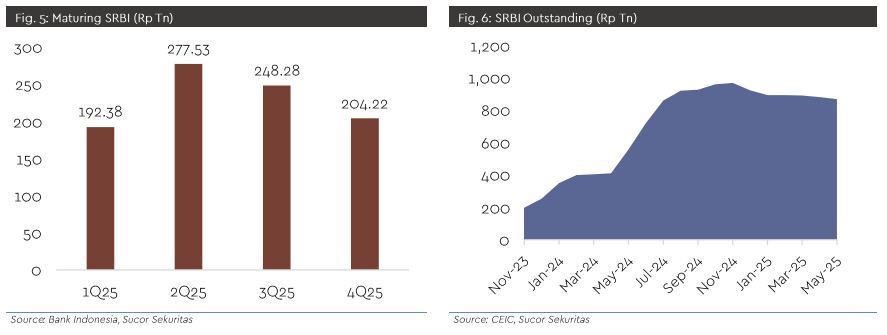

Now, a large portion of SRBI is set to mature in the second half of 2025. This opens the door for liquidity to gradually return to the system, giving banks more room to lend, optimize funding structures, and improve profitability. Outstanding SRBI has also started to decline, signaling that fewer SRBI are being issued than those maturing, a clear sign that liquidity conditions may be easing.

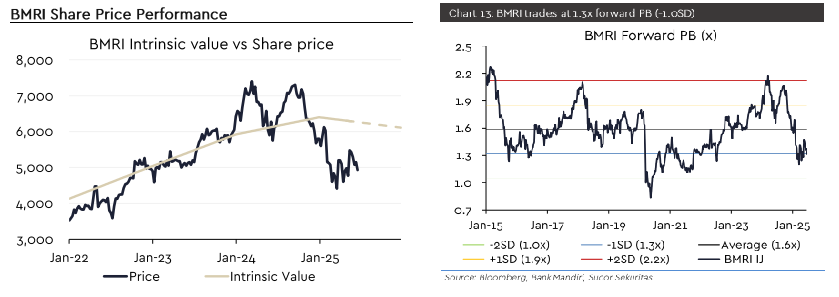

BMRI, with its strong balance sheet and consistent delivery, could be one of the early beneficiaries of this shift.

From a valuation perspective, the stock is trading at around 1.3x 25F PBV, a level that sits one standard deviation below its 10-year average. In terms of share price, it is also near its lowest levels since early 2023.

If liquidity conditions improve as SRBI matures, banks like BMRI could be among the early beneficiaries. Better funding conditions may support a healthier CASA mix, offer more flexibility in pricing, and ultimately bring back more profitable loan growth.

However, it is important to acknowledge the near-term picture. Year to date, BMRI's performance has remained flat, with total loans still at Rp1,310 trillion as of May. Although net profit reached Rp19.7 trillion and was broadly in line with our expectations, margin pressure remains, and overall loan growth has not yet picked up. With that in mind, we think its possible for the management to revise down its guidance to the market in the coming quarters.

Still, this situation is not unique to BMRI. Across the banking sector, most players are dealing with similar challenges. Liquidity has been tight, loan demand is soft, deteriorating loan quality, which resulted to pressured margin. These conditions reflect a broader industry cycle rather than a company-specific issue.

In the short term, we expect volatility to increase as the market adjusts to more cautious expectations. For long-term investors, the key is not to be discouraged by near-term softness but to focus on identifying the best entry point. As valuations become more attractive and when liquidity conditions improve, high-quality bank stocks could present compelling opportunities to gradually build positions.