Global markets ended the week on edge, with the Strait of Hormuz flipping between open and closed within a single day. On last Friday, Iran announced it was reopening the strait, sending Brent crude down nearly 10% to below USD 90/bbl, its lowest level since early March, on hopes that the most severe energy supply disruption in modern history was finally easing. That optimism proved fleeting. By Saturday, Iran reversed course, citing the continued U.S. naval blockade of Iranian ports, and shut the strait once again. Brent has since staged a modest rebound to the low USD 90s, but remains well below prior levels, and with the ceasefire due to expire on 22 April 2026, the week ahead carries material headline risk.

Against this backdrop of sustained energy volatility, the Indonesian government moved to partially pass through higher costs: Pertamina officially adjusted unsubsidised fuel prices effective 18 April. Pertamax Turbo, Dexlite, and Pertamina Dex all saw significant price increases, reflecting the prolonged pressure from elevated global crude. Subsidised fuels, namely Pertalite and Biosolar, were left unchanged, shielding lower income households from direct impact.

.png)

Source: Pertamina / MyPertamina official price list, 18 April 2026. Prices shown for DKI Jakarta region.

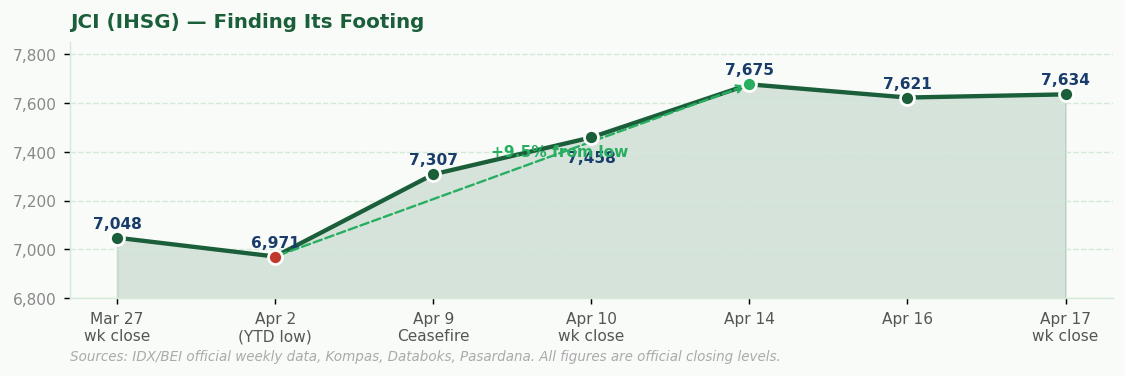

What stands out, however, is the domestic market's increasingly resilient posture. The JCI closed the week ended 17 April up +2.35% at 7,634, following the prior week's sharp +6.1% rebound from the YTD low of 6,971. Notably, on 13 April, when US-Iran talks in Islamabad failed and Trump announced a naval blockade of the strait, the JCI still closed positive while most Asian peers declined.

JCI closing levels. Sources: IDX/BEI official weekly recap, Kompas, Databoks, Pasardana. All figures are official closing levels.

The market appears to be shifting away from headline driven panic into a more selective repricing mode, focusing less on broad risk-off moves and more on identifying relative winners and losers. Domestic catalysts are helping anchor sentiment, including bank dividend season, more attractive post-correction valuations, and ongoing IDX reform momentum. The direction of US-Iran negotiations remains the key variable in determining whether this resilience can sustain.