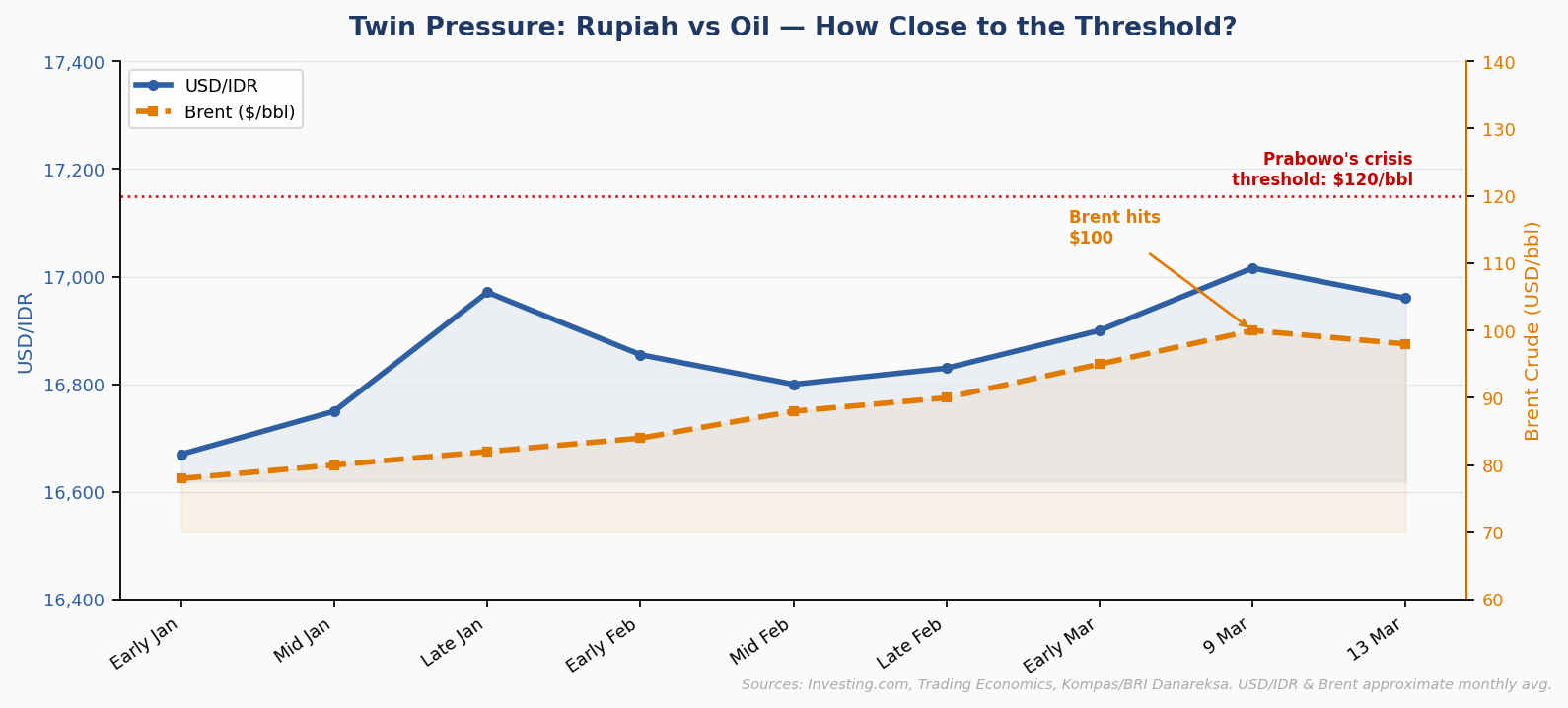

Over the weekend, markets picked up headlines about Prabowo Subianto saying Indonesia could breach its 3% of GDP fiscal deficit cap, but only in a crisis comparable to COVID, such as oil prices sustaining above $120 per barrel. On the surface this sounds like a very high bar. However, by naming the threshold, the breach scenario is no longer theoretical and now has a clear price trigger. Markets may shift from asking whether Indonesia would ever breach the rule to how close Brent is to $120. At around $98 today, the gap is roughly $22, which is not exactly a comfortable margin.

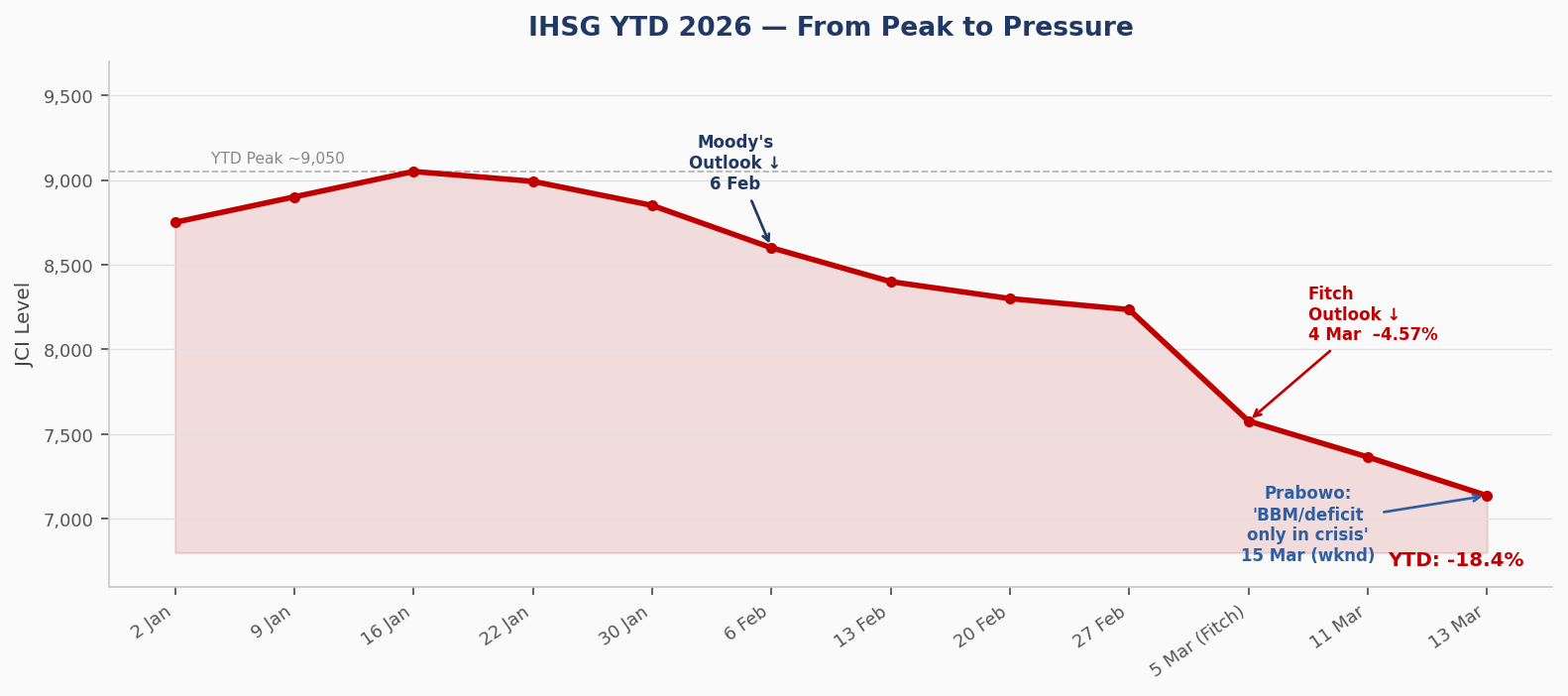

IHSG YTD 2026 — down ~18.7% from the January peak of ~9,050 to 7,137 as of 13 March. Key macro events annotated. Sources: Bloomberg, Investing.com.

Back in Jakarta, three senior officials moved quickly to deny rumors that the government is preparing a Perppu for economic intervention. Yusril Ihza Mahendra rejected the claim, the State Secretariat said no discussion had taken place, and Purbaya Yudhi Sadewa said he was unaware of any related meeting. The clarification is credible enough to calm the narrative for now, but not strong enough to fully remove market concerns. That gap between official messaging and investor confidence is where volatility tends to emerge.

Twin pressure: USD/IDR near 16,960 vs Brent at ~$98/bbl. Dotted line marks Prabowo's stated crisis threshold at $120. Sources: Trading Economics, Bloomberg.

For the IHSG, Monday’s open could see a tug of war between relief and lingering risk. The presidential statement may trigger a short covering bounce after the index fell nearly 19% from its January peak and entered oversold territory. But the broader overhang remains. Foreign outflows continue, the rupiah is still above 16,900 per dollar, and rating agencies Fitch Ratings and Moody's Investors Service still hold negative outlooks ahead of mid year reviews. A downgrade toward BBB minus remains a tail risk, but the possibility alone can limit any strong rebound.

In this environment, rotation into defensives becomes the more relevant conversation rather than taking a broad index view. Telcos stand out as a cleaner pocket, as their revenues and costs are largely domestic and they have limited exposure to oil prices or fiscal policy risk. With stable ARPU trends and potential 5G monetization, the sector offers clearer earnings visibility for investors who want Indonesia exposure without taking full market beta.