14 July 2026

Rating Held, Yield Gap in Focus

Market Commentary

0 comments

Global markets remain jittery, with the US reinstating a blockade on Iranian shipping through the Strait of Hormuz, sending Brent crude past $84 and Asian equities broadly lower. Against that backdrop, IHSG stood out — closing today (14/7) at 6,039.52, holding above the psychological 6,000 level after Monday's 1.92% surge on S&P Global Ratings affirming Indonesia's BBB/A-2 rating with a stable outlook. S&P still expects 5.1% growth in 2026 and a fiscal deficit held under 3.0% of GDP, helped by 21.4% yoy H1 state revenue growth, even as the free-meals (MBG) program gets trimmed by roughly a third.

S&P was explicit on what would flip the outlook negative: net government debt rising more than 3% of GDP a year on a sustained basis, interest payments staying above 15% of revenue for good, or export receipts slowing structurally enough to push external financing needs consistently above the sum of current account receipts and usable reserves. None of these are S&P's base case today — but they're the lines to watch. S&P also flagged Danantara Sumberdaya Indonesia's (DSI) crackdown on underinvoicing and transfer pricing as a constructive, revenue-supportive step.

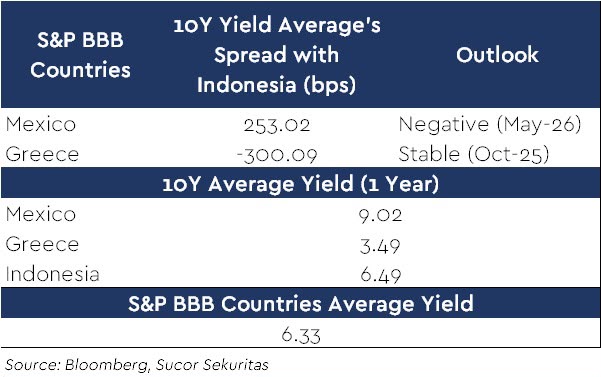

The re-rating trigger we're watching is the yield gap. Indonesia's 10Y still trades well above the BBB-peer average (~6.33%). A meaningful compression could unlock Rp100tn–Rp300tn in foreign inflows into IDR bonds — a strong tailwind for the rupiah and equities. Worth noting: foreign investors booked a net sell of around Rp412 billion today, meaning the rally so far is domestically driven rather than foreign-flow-led — the real test comes once global risk-off (Hormuz, oil, Fed) eases and foreign capital follows. No fresh stock pick for now, bias stays toward rupiah- and rate-sensitive names as the spread narrows.

S&P was explicit on what would flip the outlook negative: net government debt rising more than 3% of GDP a year on a sustained basis, interest payments staying above 15% of revenue for good, or export receipts slowing structurally enough to push external financing needs consistently above the sum of current account receipts and usable reserves. None of these are S&P's base case today — but they're the lines to watch. S&P also flagged Danantara Sumberdaya Indonesia's (DSI) crackdown on underinvoicing and transfer pricing as a constructive, revenue-supportive step.

The re-rating trigger we're watching is the yield gap. Indonesia's 10Y still trades well above the BBB-peer average (~6.33%). A meaningful compression could unlock Rp100tn–Rp300tn in foreign inflows into IDR bonds — a strong tailwind for the rupiah and equities. Worth noting: foreign investors booked a net sell of around Rp412 billion today, meaning the rally so far is domestically driven rather than foreign-flow-led — the real test comes once global risk-off (Hormuz, oil, Fed) eases and foreign capital follows. No fresh stock pick for now, bias stays toward rupiah- and rate-sensitive names as the spread narrows.

Written by Boris, the Broker

Comments