23 February 2026

The Beginning of A Robust Growth

Market Commentary

0 comments

PT Solusi Sinergi Digital Tbk (WIFI) has been one of our preferred stock picks in recent months, as we believe the company offers substantial untapped growth potential at an attractive valuation. A key catalyst for future upside is its Internet Rakyat initiative, which aims to deliver affordable broadband access across Indonesia through 5G Fixed Wireless Access (FWA) technology.

Following its successful acquisition of the 1.4 GHz spectrum, WIFI has begun rolling out this service without requiring fiber-optic installation to individual households. By eliminating costly last-mile cable deployment, the company can accelerate network expansion and customer acquisition compared with traditional fiber-based competitors.

Currently, it is riced at IDR 100k/month for speeds up to 100 Mbps with unlimited data. The current pricing reflects its affordable “Internet Rakyat” positioning. Under the prevailing regulatory framework, WIFI retains the flexibility to adjust its tariffs up to IDR 147,000 per month, thereby providing strategic optionality for future ARPU optimization.

Management has set a target of reaching 5 million active subscribers by December 2026, underpinned by the deployment of approximately 5,493 network sites by the end of the year. Capex per site is projected at around US$30,000, with each location designed to accommodate roughly 1,000 subscribers.

On a per-home connection basis, the required capital investment is estimated at approximately IDR 1.3 million. This consists of around IDR 825,000 allocated for CPE and approximately IDR 528,000 for RAN infrastructure components.

.jpeg)

We project 4Q25 EBITDA and net profit at Rp199bn and Rp128bn, respectively. The uplift is driven by advertising turning profitable as ad slots were monetized externally, alongside subscriber-led revenue growth. Spectrum-related FWA fees will only be recognized from 2026 onward, hence not impacting 4Q25 earnings.

Supported by a projected 10-year subscriber CAGR of 33%, bringing the user base to 25 million, the company is anticipated to achieve revenue growth of 40% CAGR over the same period, reaching IDR 45tn. Over the long term, we estimate average net and operating margins of 29% and 50%, respectively, driven by strong operating leverage and improved scale efficiencies. Therefore, we reiterate our buy call with TP of IDR 9,500.

Following its successful acquisition of the 1.4 GHz spectrum, WIFI has begun rolling out this service without requiring fiber-optic installation to individual households. By eliminating costly last-mile cable deployment, the company can accelerate network expansion and customer acquisition compared with traditional fiber-based competitors.

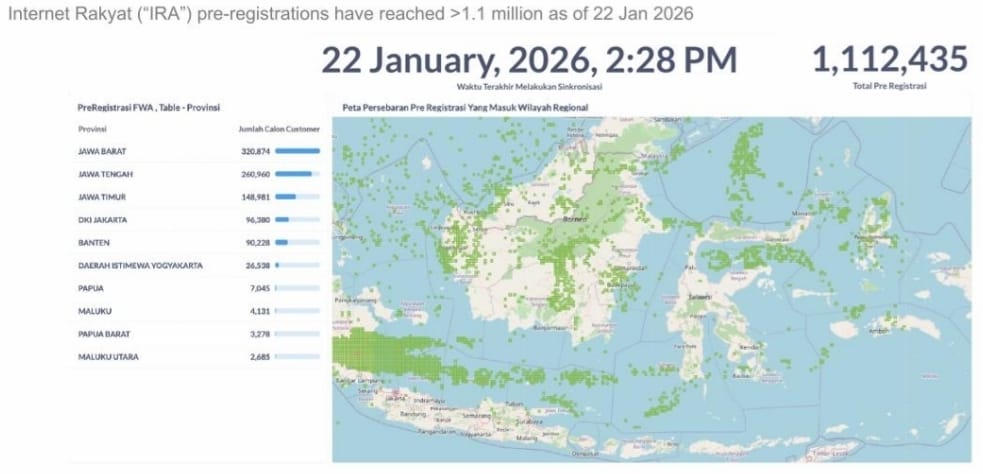

Internet Rakyat Pre-registration

Currently, it is riced at IDR 100k/month for speeds up to 100 Mbps with unlimited data. The current pricing reflects its affordable “Internet Rakyat” positioning. Under the prevailing regulatory framework, WIFI retains the flexibility to adjust its tariffs up to IDR 147,000 per month, thereby providing strategic optionality for future ARPU optimization.

Management has set a target of reaching 5 million active subscribers by December 2026, underpinned by the deployment of approximately 5,493 network sites by the end of the year. Capex per site is projected at around US$30,000, with each location designed to accommodate roughly 1,000 subscribers.

On a per-home connection basis, the required capital investment is estimated at approximately IDR 1.3 million. This consists of around IDR 825,000 allocated for CPE and approximately IDR 528,000 for RAN infrastructure components.

WIFI's Home Pass and cumulative subscriber

We project 4Q25 EBITDA and net profit at Rp199bn and Rp128bn, respectively. The uplift is driven by advertising turning profitable as ad slots were monetized externally, alongside subscriber-led revenue growth. Spectrum-related FWA fees will only be recognized from 2026 onward, hence not impacting 4Q25 earnings.

Supported by a projected 10-year subscriber CAGR of 33%, bringing the user base to 25 million, the company is anticipated to achieve revenue growth of 40% CAGR over the same period, reaching IDR 45tn. Over the long term, we estimate average net and operating margins of 29% and 50%, respectively, driven by strong operating leverage and improved scale efficiencies. Therefore, we reiterate our buy call with TP of IDR 9,500.

Written by Boris, the Broker

Comments