In our previous sales note, we discussed why PRDL stands out from a business and fundamental perspective. This time, we believe its valuation is another compelling aspect of the investment case. At the IPO price range of Rp100–120 per share, PRDL is offered at around 10–12x FY26F P/E, providing an attractive entry valuation for a profitable company operating in Indonesia's healthcare diagnostics sector.

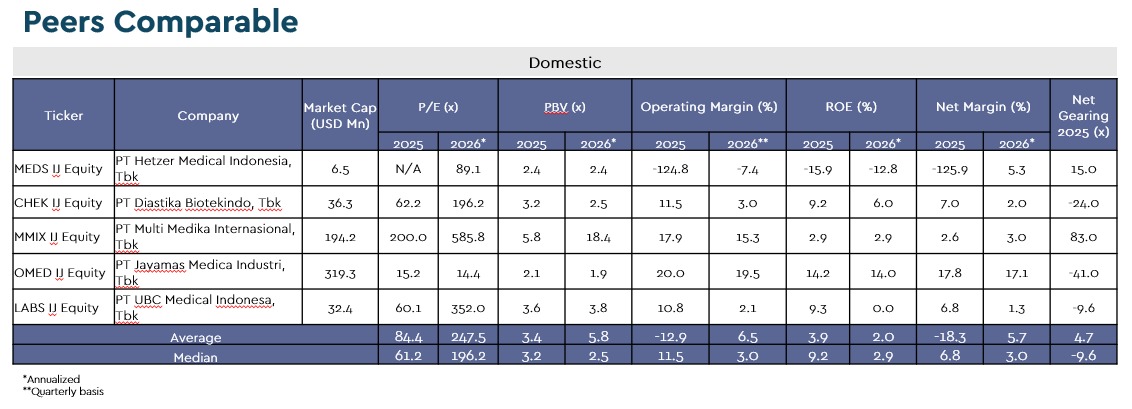

Compared with listed diagnostics peers, PRDL's IPO valuation stands below most comparable companies. While several peers currently trade at significantly higher earnings multiples, PRDL already operates a profitable business, owns its manufacturing facilities, and has established a strong position in the domestic market. In our view, this leaves room for potential valuation rerating as the company continues to deliver earnings growth after listing.

Beyond its attractive valuation, PRDL is also entering an earnings monetization phase. The company has largely completed its major capital investment cycle, with most of the spending on production facilities already behind it. Going forward, capital expenditure is expected to normalize, allowing future revenue growth to translate into stronger operating leverage and faster earnings growth as existing production capacity is further utilized.

The public offering period has officially commenced and will run through 7 July 2026, ahead of the company's expected listing on 9 July 2026. For investors seeking exposure to Indonesia's healthcare sector, PRDL offers an attractive entry valuation relative to listed diagnostics peers.