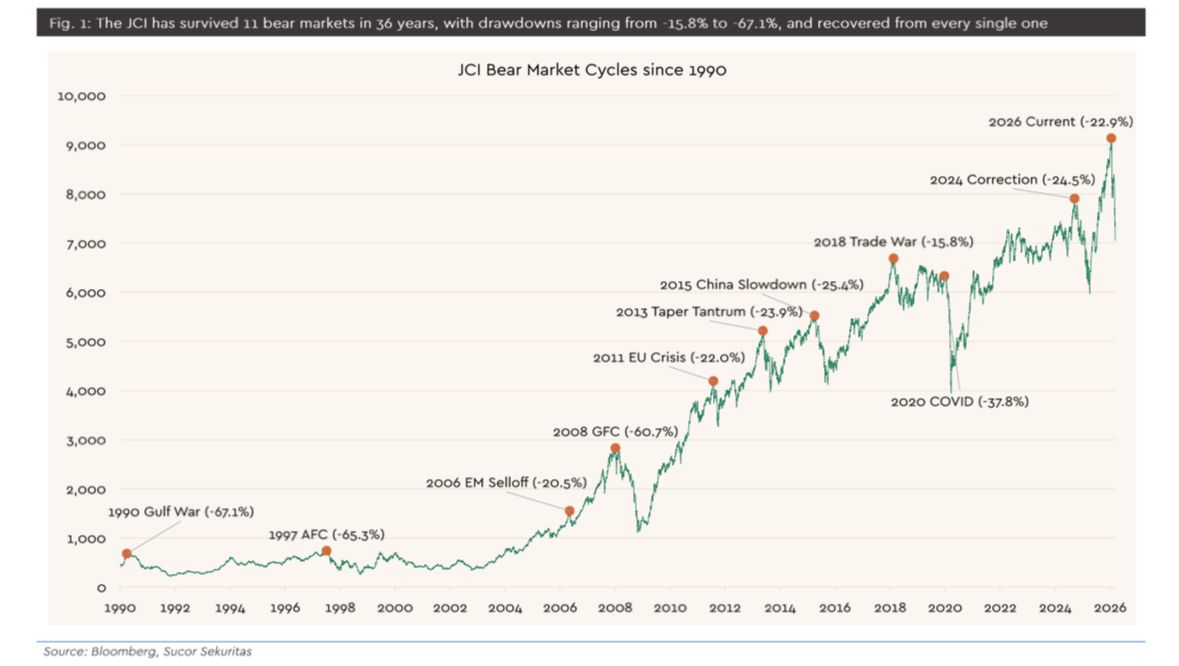

The Jakarta Composite Index (JCI) has declined 22.9% from its January 2026 peak, officially entering a bear market. While the speed of the selloff—occurring within just 55 trading days—is among the fastest in history, the magnitude still falls within the range of a moderate correction (-16% to -26%), rather than a systemic crisis. Historically, deeper crises such as 1997 and 2008 saw drawdowns exceeding -60%, indicating that current conditions have not yet reached structural breakdown territory.

The current weakness is driven by a convergence of multiple risk factors. On the external side, geopolitical tensions in the Middle East have pushed oil prices higher, creating pressure on inflation and fiscal balances. Domestically, concerns around a potential sovereign rating downgrade, MSCI index risks, and Rupiah depreciation are weighing on capital flows and investor sentiment. Additional risks such as fuel price hikes could further weaken consumption and corporate earnings. Unlike typical corrections driven by a single trigger, this environment reflects overlapping and interlinked risks, making the outlook more uncertain.

.jpeg)

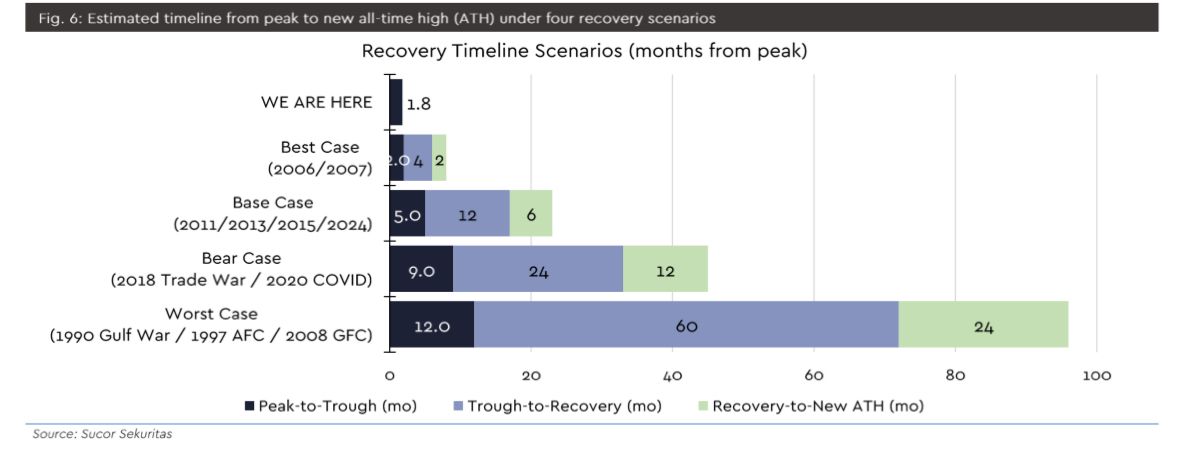

From a timing perspective, the correction appears to still be in its early phase, having lasted only around 1.8 months compared to a historical median of 4.4 months. This suggests that near-term volatility may persist, and the market may not have fully bottomed yet. Based on historical scenarios, a moderate extension could bring the JCI toward 6,300–6,400, while a more severe (but still non-crisis) scenario could push it closer to 5,500. A full systemic crisis scenario remains low probability, unless current risks escalate into a broader macroeconomic deterioration.

Despite short-term uncertainty, long-term patterns remain constructive. Across all past cycles, the JCI has consistently recovered and reached new all-time highs. Moderate corrections typically see recovery within 6–18 months, with the next peak often 20–30% higher than the previous one. This reflects Indonesia’s structural growth drivers, including strong demographics, expanding domestic consumption, and natural resource strength. As a result, while the current phase may remain volatile, it still aligns with a broader pattern where market corrections create opportunities within a long-term uptrend.