Since the early hours of March 1, 2026, the global shipping world has been holding its breath. Following coordinated U.S.-Israeli strikes on Iran under Operation Epic Fury, the Strait of Hormuz, the jugular vein of global energy trade, has effectively ground to a standstill. Tanker transits collapsed by over 80% in a matter of days. VLCC benchmark freight rates hit an all-time record of USD 423,736/day. Marine war-risk insurers including Gard, Skuld, and London P&I Club have pulled coverage entirely for vessels in the Persian Gulf. The world is watching the most significant maritime disruption since the COVID era, and possibly since World War II.

.jpeg)

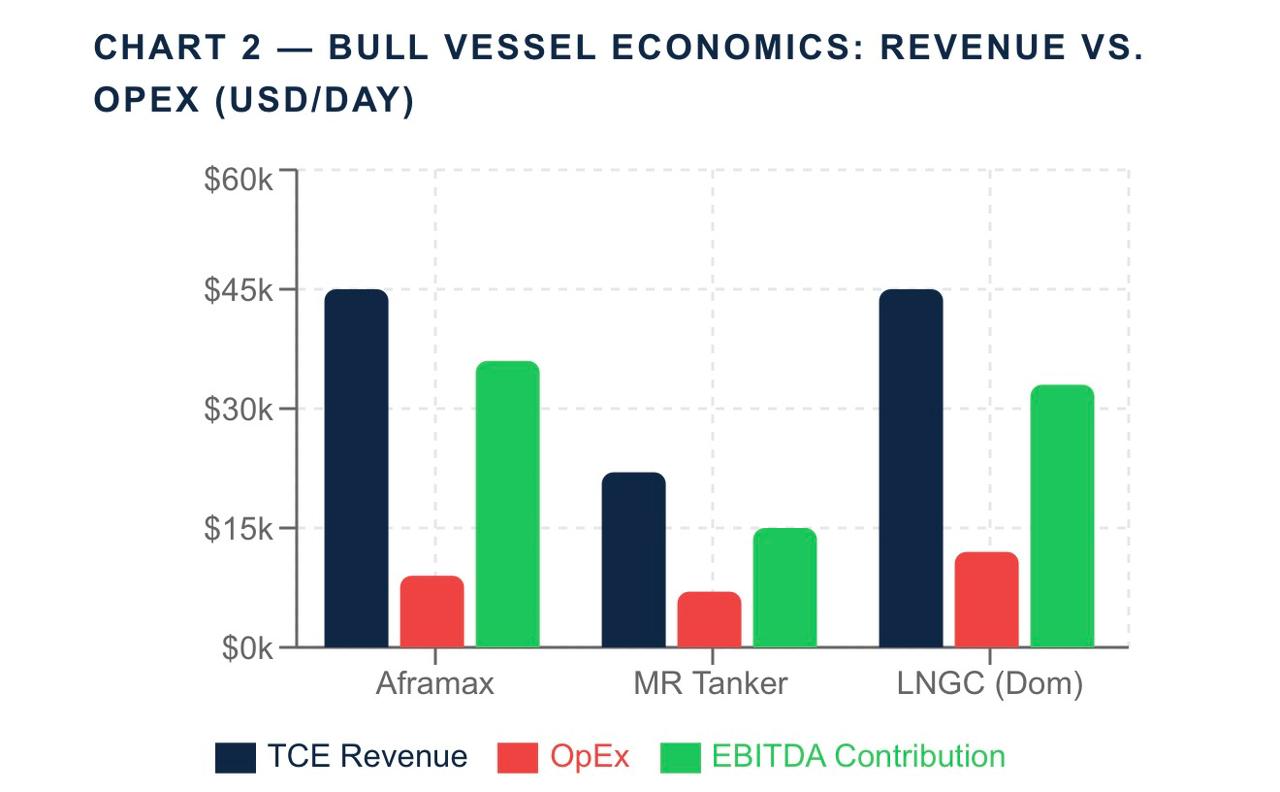

Against this backdrop, one question stands out for Indonesia based investors: which listed company is best positioned to benefit? The answer, we believe, is PT Buana Lintas Lautan Tbk (BULL), a shipping company whose fleet is strategically deployed outside the Hormuz corridor, yet is seeing its charter rates lifted materially by the global supply shock. BULL's 10-vessel fleet, comprising 3 Aframax, 5 MR tankers, 1 LNG carrier, and 1 LPG carrier, is currently positioned across South America, North America, Africa, Europe, Turkey, South Korea/China, and Indonesia, none of them stuck in the Persian Gulf.

The global oil tanker market was already structurally tight before this crisis. Approximately 20% of the global fleet had been sanctioned, 17% of vessels were tied up in the Persian Gulf, and newbuild deliveries remain limited until late 2026 at the earliest. The Hormuz closure is essentially a demand shock on top of a pre-existing supply constraint, and BULL, operating entirely on spot charter, is a direct beneficiary of every dollar of rate upside.

Beyond the tanker thesis, BULL is quietly building one of the most compelling LNG carrier businesses in Indonesia's domestic market. With the nearest LNGC delivery expected March/April 2026, and a pipeline of FSRU and FPSO tenders that could contribute meaningfully from 2027–2028, BULL is evolving from a pure tanker play into a multi-segment energy shipping platform. The company's rights issue (PMHMETD) planned for 2H26 will further capitalize the balance sheet to fund an accelerated fleet expansion, targeting DER of 2.0x from just 0.6x currently.

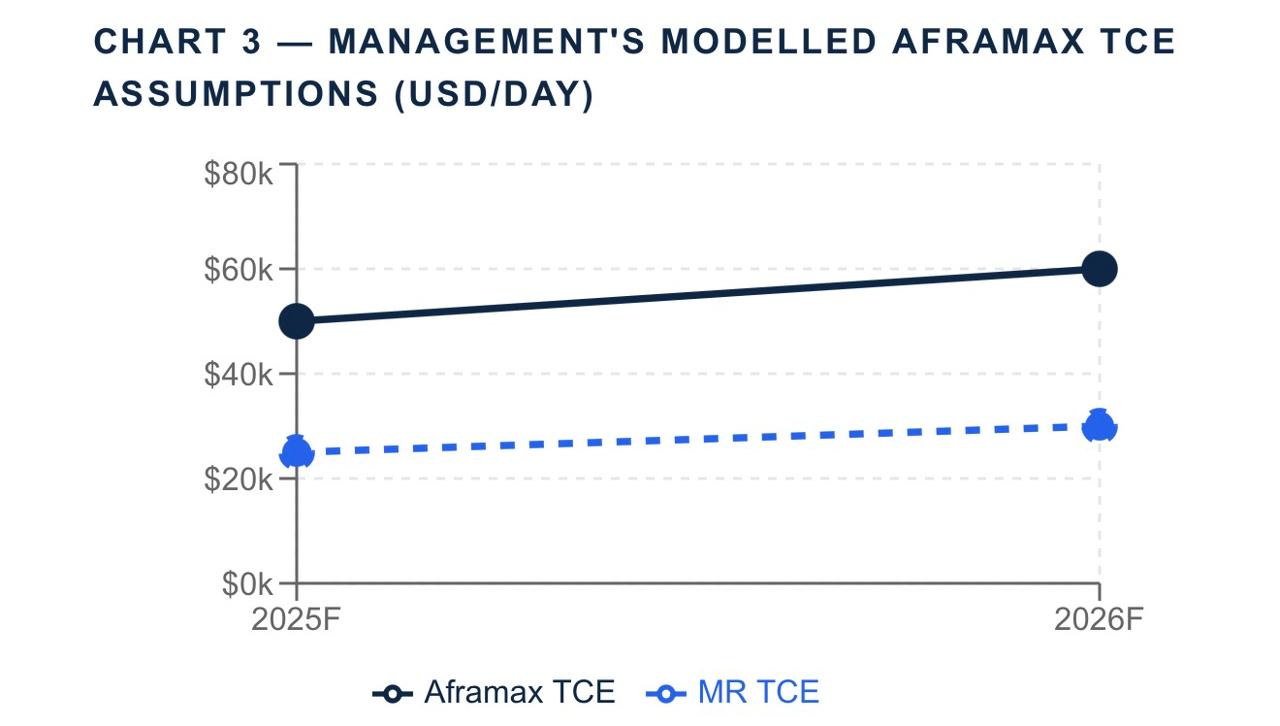

Note: Management's conservative modelling assumptions are well below current spot, significant upside optionality.

Management's 2025F Aframax TCE assumption of USD 50k/day and 2026F at USD 60k/day appear deeply conservative against current spot of USD 100k/day. Each USD 10k/day increment above assumption across 3 Aframax vessels translates to meaningful incremental quarterly EBITDA.

Furthermore, BULL's next LNGC delivery is March/April 2026, with a target of 3–4 vessels by end-2026. Currently, Indonesia has ~8 domestic LNGC vessels, of which 4 are locked on time charter, leaving just 4 competing on spot tenders from Pertamina, PLN, and PGN. Domestic TCE of USD 40–50k/day against opex of USD 11–12k/day implies margins of 70–75%.

We think this is a timely moment to revisit BULL, not just as a tactical trade on Hormuz disruption, but as a structurally underappreciated shipping company with earnings power, asset value, and a long-term growth pipeline that the market has yet to fully price in.