During my recent visits to client meeting rooms, I noticed something intriguing: most of them provided CLEO mineral water. I couldn’t miss it, the bright orange bottle really stands out!

Turns out, there’s been a noticeable shift lately. Local bottled water brands like CLEO is gaining traction. This comes amid a wave of boycotts against some foreign brands owned by multinational companies.

They mentioned that this boycott has created a unique opportunity for local brands.

CLEO has two main segments: bottled water, contributing 55% of its revenue, and non-packaged water, which accounts for 44%.

Interestingly, the non-packaged segment offers higher profit margins, 63% compared to 56% for the bottled segment.

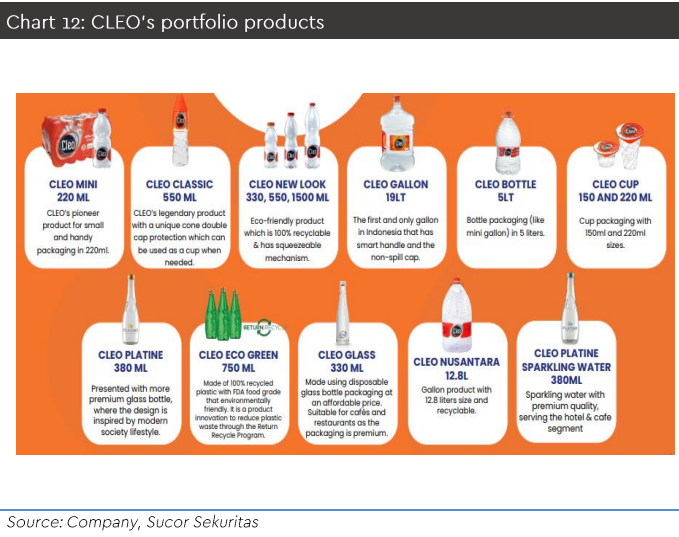

CLEO is also constantly innovating, offering a variety of sizes and even premium products like glass bottles for the Horeca (Hotels, Restaurants, Cafes) industry.

These glass bottles, while giving a luxurious vibe, are surprisingly affordable at just around IDR 7,000/bottle.

What sets CLEO apart is its focus on pure water rather than mineral water. Using advanced nano-filtration technology with ultra-small membranes of just 0.0001 microns, CLEO delivers water with 99.99% purity.

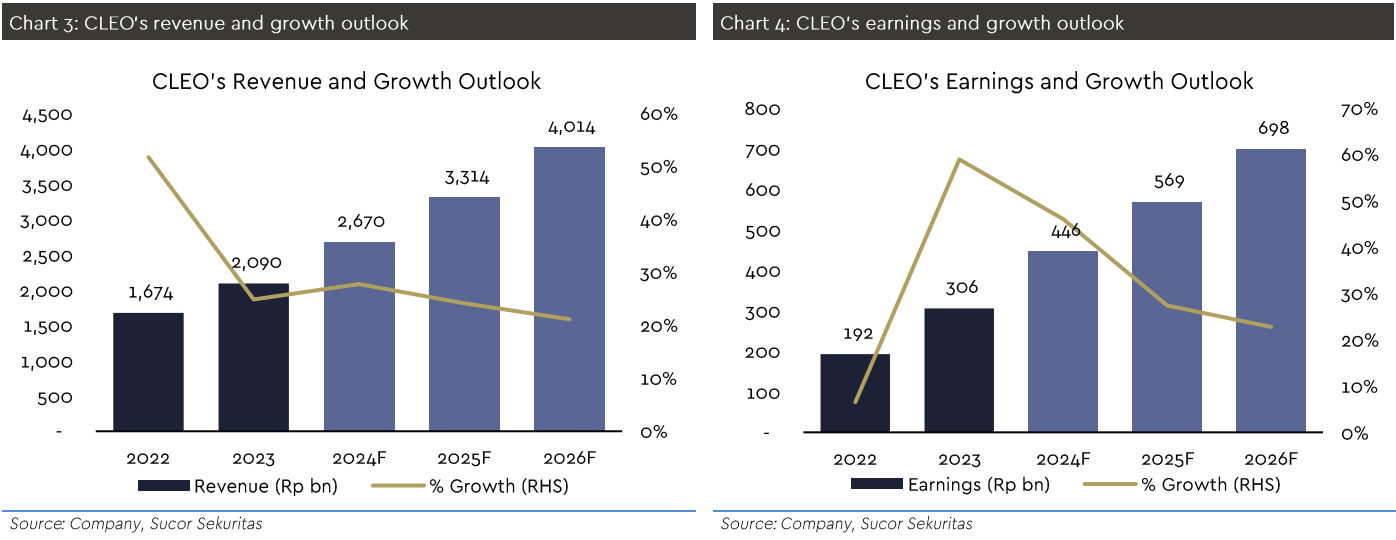

This unique approach has driven CLEO’s rapid growth in the bottled water industry, with average revenue growth of 20% and profit growth of 37% annually over the past five years. As of September 2024, their market share has climbed to 7%, up from less than 4% in 2018.

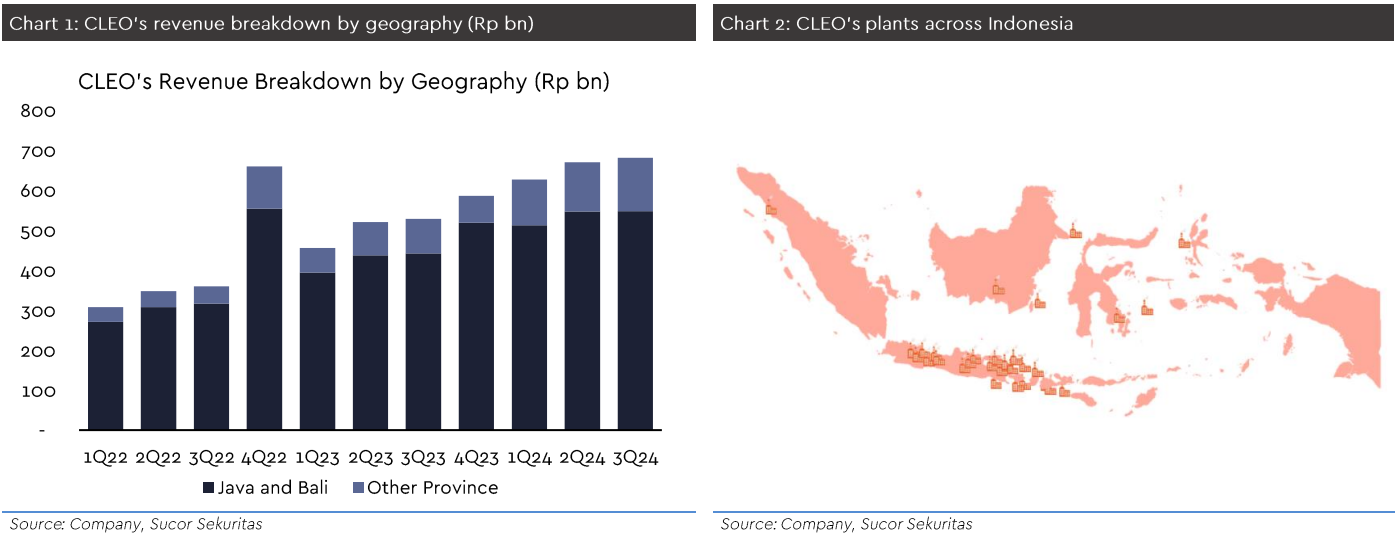

The secret to their success? Aggressive manufacturing and distribution. CLEO operates 32 plants, mostly in Java and Bali, which together contribute 81% of total sales.

They plan to add three new plants in Palu, Pontianak, and Pekanbaru, each boosting production capacity by 100 mn liters annually. Their ultimate goal is to reach 50 plants by 2030, effectively doubling their production capacity.

CLEO is projected to maintain strong profit growth at an average of 26% annually over the next five years.

Revenue is also expected to grow by 21% annually, driven by increased sales volumes supported by capacity expansion.

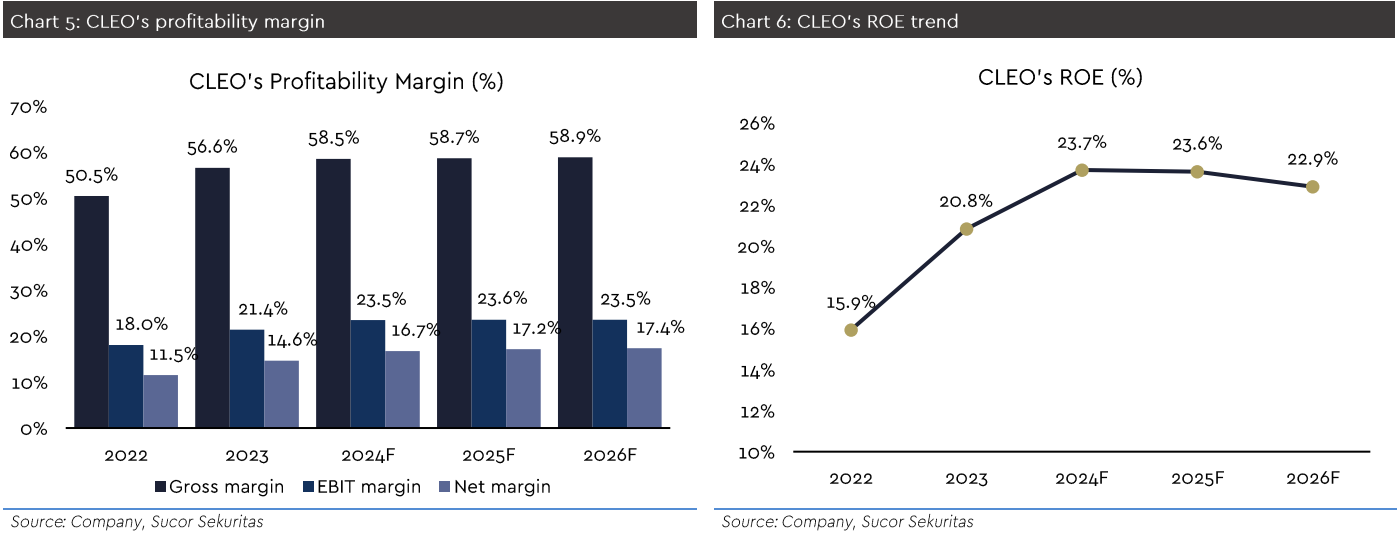

GPM and NPM are forecasted to rise to 58.9% and 17.4%, respectively, thanks to improved plant efficiency and annual price increases of 3-5%.

Distribution is CLEO’s competitive edge.

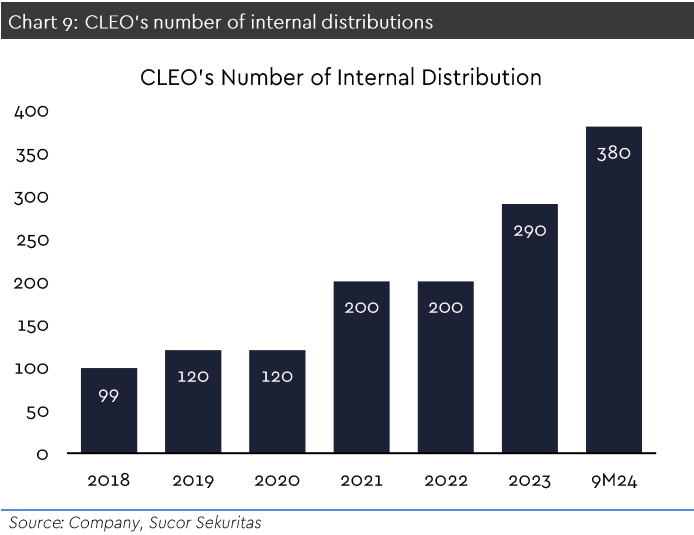

They operate through two main channels: their subsidiary, PT Sentrasari Primasentosa (SPS), with 380 internal distribution points, and over 7,000 external distribution partners. This strategy allows CLEO to quickly and efficiently reach a wide market.

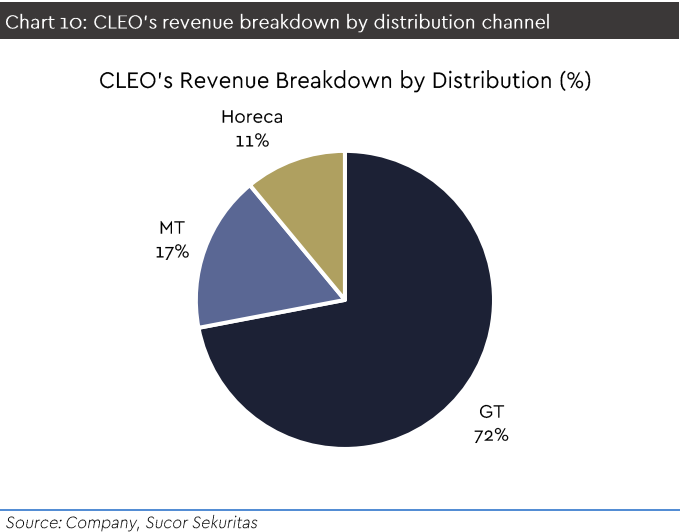

Currently, 72% of CLEO’s products are sold through GT, 17% through MT, and 11% through Horeca channels.

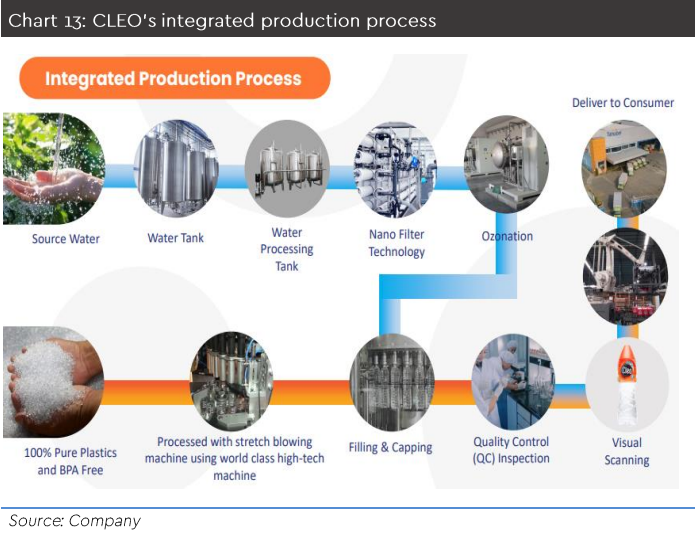

Another key strength lies in CLEO’s fully integrated production and distribution process. From water processing, filling, and packaging to delivery, everything is managed in-house. Even the plastic bottles, gallons, labels, and packaging materials are produced by CLEO itself.

This integration significantly reduces reliance on third party suppliers, cutting costs and ensuring consistent quality. By controlling every aspect of its operations, CLEO has built a strong position in the market.

With such a positive outlook, we recommend a BUY with a target price of IDR 1,510. CLEO is well-positioned for continued growth and market dominance!