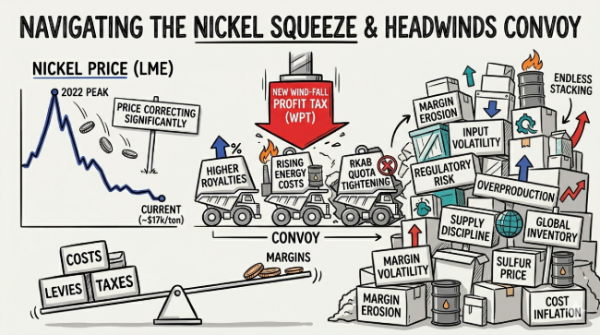

Last week, we saw headlines around the government’s plan to introduce additional levies on the nickel industry, potentially taking effect as early as April 2026. The move is part of efforts to strengthen state revenues and keep the fiscal deficit under control amid rising global oil prices and ongoing Middle East tensions. While the final structure is still being formulated, the policy direction points toward a more progressive mechanism tied to commodity prices, potentially aligning with broader policy goals such as downstreaming and supply discipline in the global nickel market if implemented. However, the timing could be challenging given nickel prices have already corrected significantly from their 2022 peak, leaving industry margins more compressed and financial buffers relatively thinner.

.png)

This pressure is compounded by a series of overlapping headwinds already facing the sector, including higher royalty rates implemented since April 2025, a sharp increase in energy costs, and tighter approval processes for the 2026 RKAB quotas. At the same time, production discipline appears to be tightening as authorities aim to rebalance an oversupplied global market. The combination of controlled volumes and rising input costs, particularly sulfur, suggests that cost pressures are building just as additional fiscal measures are being introduced.

.png)

.png)

On the ground, Vale Indonesia (INCO) appears relatively resilient, supported by its efficient cost structure as an integrated operator. The company recently reported a solid increase in net profit for 2025 despite lower average selling prices, with additional support coming from saprolite ore sales helping to cushion cash flows. Meanwhile, Harita Nickel (NCKL) continues to push aggressive volume growth across its NPI and HPAL segments to sustain expansion momentum. However, with production costs still exposed to input price volatility, particularly sulfur, and fiscal incentives evolving over time, margin trajectory will remain a key area of focus for the market as the progressive levy framework takes shape.

Overall, the sector is entering a more complex phase where policy, cost inflation, and supply discipline are converging, making margin sustainability rather than just volume growth the key differentiator to watch across nickel names going forward.