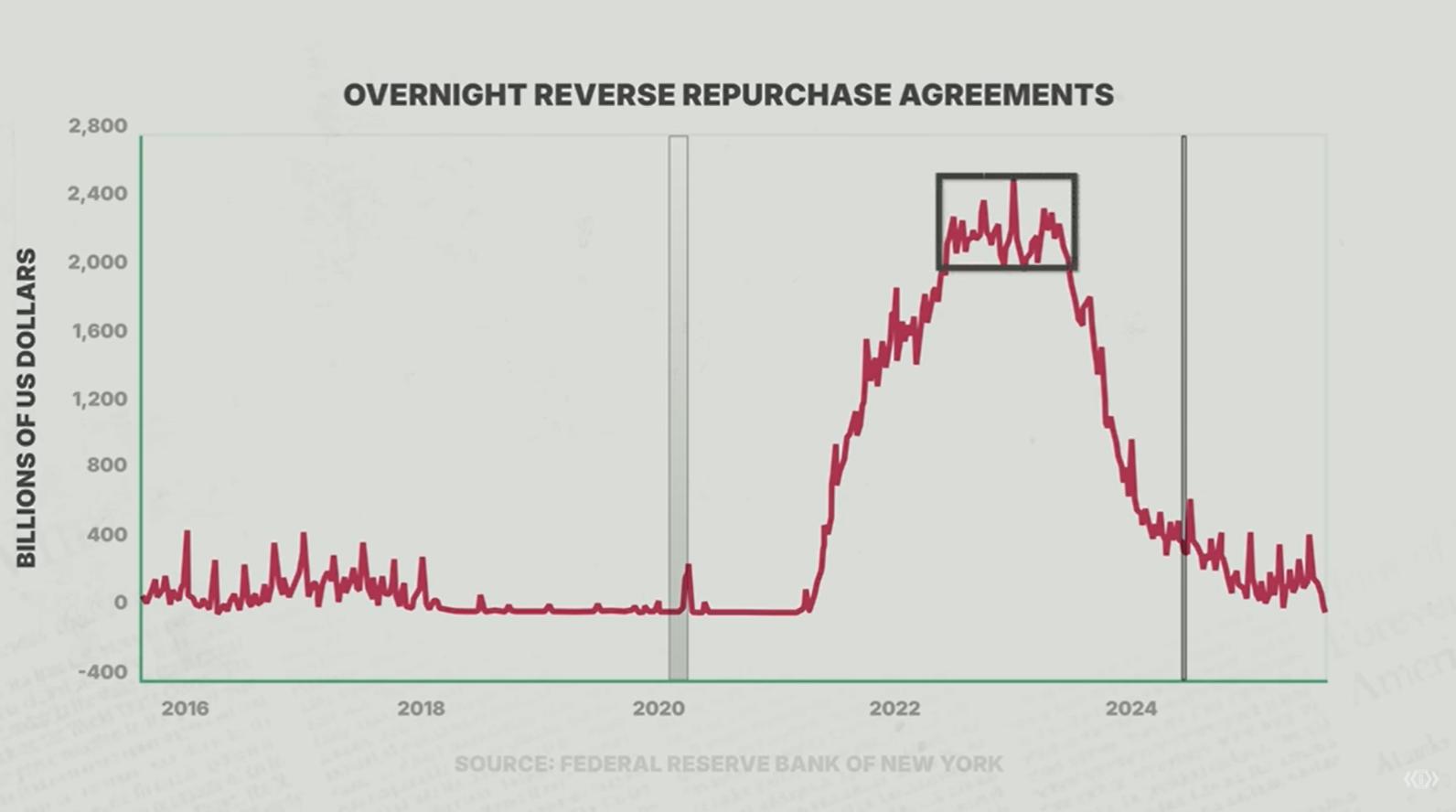

We’ve seen a similar case in 2020 when extra liquidity went into the Fed’s reverse repo facility, which grew to USD 2.5 trillion. But once T-bill yields went higher than the repo rate, money shifted away and the balance is now nearly zero.

The same thing could happen now. If bank reserves stop earning interest, funds will likely move into Treasuries. Since the U.S. is still borrowing heavily, this inflow could push yields lower, tighten EM spreads, and bring benefits to Indonesia through bonds, the rupiah, and equities.

Meanwhile, all eyes are on the September 17 Fed meeting, where rate cuts are back in play. If the Fed cuts aggressively, it could steepen the curve, send real rates negative, and spark a “Goldilocks rally” where bonds, EM assets, equities, and commodities all rise together. For Indonesia, this could mean more foreign inflows and stronger performance in banks, gold, and commodity-related stocks.

We prefer BBCA and BBRI. Historically, foreign investors tend to return to BBCA first, making it a natural proxy for foreign appetite. On the other hand, BBRI looks attractive because its foreign ownership has fallen from previous highs, creating more space for re-entry. In addition, BBRI has built a strong provision buffer, as seen in its relatively high loan loss reserve ratio. This not only provides downside protection but also opens room for earnings recovery as credit costs normalize.

.png)

Gold also looks attractive. Negative real rates and excess liquidity make it a strong hedge, with BRMS as a direct play. A weaker dollar could also trigger a broad commodity rally, helping exporters and boosting the case for commodity-linked names.

In short, whether through the FAR Act or a Fed pivot, the story is the same: global liquidity is coming back, and Indonesia is right in the middle of it.