22 August 2025

From diesel steady to turbo ready

Market Commentary

0 comments

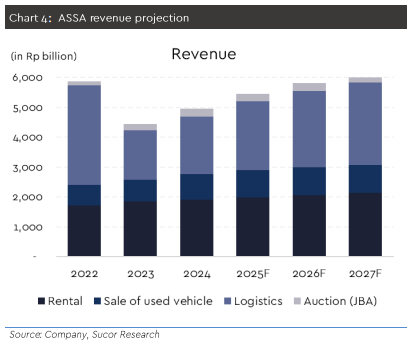

In the past, when people thought of ASSA, the image was always about car rentals. A diesel engine that is steady, consistent, and reliable, keeping the company moving forward year after year. Over time this business has grown around 4% annually and still contributes close to 40% of revenue. It may not be the flashiest story, but it is the foundation that keeps ASSA running smoothly.

Today a second engine has been switched on, and that is logistics. This is not just an add-on but a turbo that is starting to carry most of the weight. In 1H25, logistics revenue grew 16% yoy, margins expanded to 10.6% from 6.8%, and the segment already accounts for 43% of operating profit. The Samperona project, set to be fully operational in 2026, will add about Rp300bn capacity each year. The turbo is not even at full boost yet.

.png)

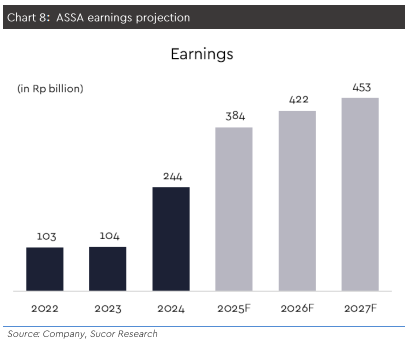

This twin-engine setup completely changes the picture for ASSA. Rentals remain the calm and steady diesel, while logistics provides acceleration with much stronger margins. As a result, 2025 earnings are projected to soar 80% yoy to Rp381bn, supported by logistics growth, higher SPX tariffs, and improving efficiency.

ASSA is switching from steady drive to full throttle. Rental keeps the cash engine steady, but logistics is stepping on the gas with faster growth and fatter margins. With both engines firing, earnings are set to accelerate and the road ahead looks wide open. At Rp1,400 target price, there is still plenty of upside fuel in the tank.

Today a second engine has been switched on, and that is logistics. This is not just an add-on but a turbo that is starting to carry most of the weight. In 1H25, logistics revenue grew 16% yoy, margins expanded to 10.6% from 6.8%, and the segment already accounts for 43% of operating profit. The Samperona project, set to be fully operational in 2026, will add about Rp300bn capacity each year. The turbo is not even at full boost yet.

This twin-engine setup completely changes the picture for ASSA. Rentals remain the calm and steady diesel, while logistics provides acceleration with much stronger margins. As a result, 2025 earnings are projected to soar 80% yoy to Rp381bn, supported by logistics growth, higher SPX tariffs, and improving efficiency.

ASSA is switching from steady drive to full throttle. Rental keeps the cash engine steady, but logistics is stepping on the gas with faster growth and fatter margins. With both engines firing, earnings are set to accelerate and the road ahead looks wide open. At Rp1,400 target price, there is still plenty of upside fuel in the tank.

Written by Boris, the Broker

Comments