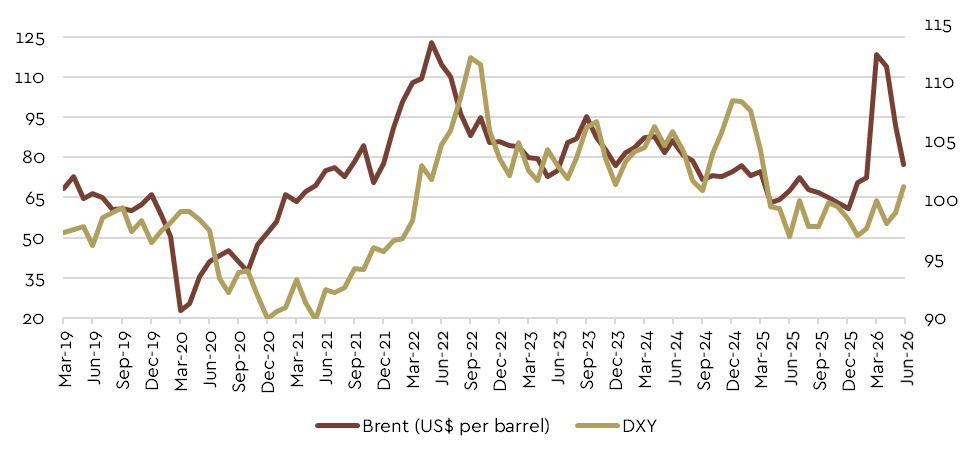

The Fed remains at the center of market debate, with growing concerns that it may be “behind the curve” as US growth signals soften while policy remains relatively restrictive. The US dollar’s strength over recent years has been supported by elevated oil prices driven by geopolitical tensions and higher US Treasury yields reflecting fiscal expansion. However, easing oil prices are now weakening one key support for the dollar, while persistently high yields continue to tighten financial conditions, weighing on US equities and broader economic activity. The narrowing 2s10s spread (~25bps) further signals cautious growth expectations. Against this backdrop, expectations are building for potential Fed rate cuts in 3Q26. Such a shift would likely ease global financial conditions, weaken the US dollar, and provide support for emerging market assets, including the rupiah. In the near term, this opens room for IDR appreciation toward Rp17,400–17,600, though seasonal FX pressures may re-emerge in 4Q26 due to import demand and other flows.

Domestically, the government has announced a Rp26.34 trillion stimulus package for 2H26, consisting of transportation incentives, food assistance, vocational training, and apprenticeship programs aimed at supporting household purchasing power and economic activity. While the package is relatively small compared to Indonesia’s overall economic size, its targeted nature could help sustain consumption and support labor-intensive industries. The move also reflects the government's effort to balance fiscal discipline with growth support amid ongoing external uncertainties.

Meanwhile, market attention remains firmly focused on the upcoming MSCI market review, which will determine whether Indonesia retains its Emerging Market (EM) status or faces the risk of a downgrade. The outcome is particularly important as it could significantly influence foreign fund flows into Indonesia. While a retention of EM status would likely support investor confidence, any negative outcome could trigger additional foreign outflows and prolong market volatility.

.png)

Amid continued macro uncertainty, we favor companies with strong balance sheets and the ability to capitalize on industry dislocations. In this regard, Barito Pacific Tbk stands out as a key beneficiary of the ongoing regional petrochemical consolidation cycle. With US$2.9bn in cash and access to offshore funding channels, BRPT is well positioned to acquire distressed assets at attractive valuations and expand its competitive moat. Supported by the strong growth trajectory of Aster, consolidated revenue is projected to grow at a 21% CAGR over 2025–28F, reaching US$13bn by 2028, while earnings are expected to improve significantly from a loss position in 2025 to approximately US$1.0bn by 2028. We continue to view BRPT as an attractive long-term consolidation play.