Our economist sees Indonesia's macroeconomic environment becoming increasingly challenging amid a weaker rupiah at Rp18,187/USD, May inflation accelerating to 3.08% YoY, and Bank Indonesia raising its benchmark rate to 5.50% in two consecutive months. These measures highlight BI's commitment to maintaining currency and inflation stability, although they may weigh on economic growth, which we expect to moderate to 4.8% in 2026.

.png)

The impact on equities is likely to be mixed. Consumer, retail, and import-dependent companies may face pressure from weaker purchasing power and rising costs, while banks could benefit from stronger NIMs. Commodity exporters meanwhile continue to enjoy the advantages of USD-denominated revenues.

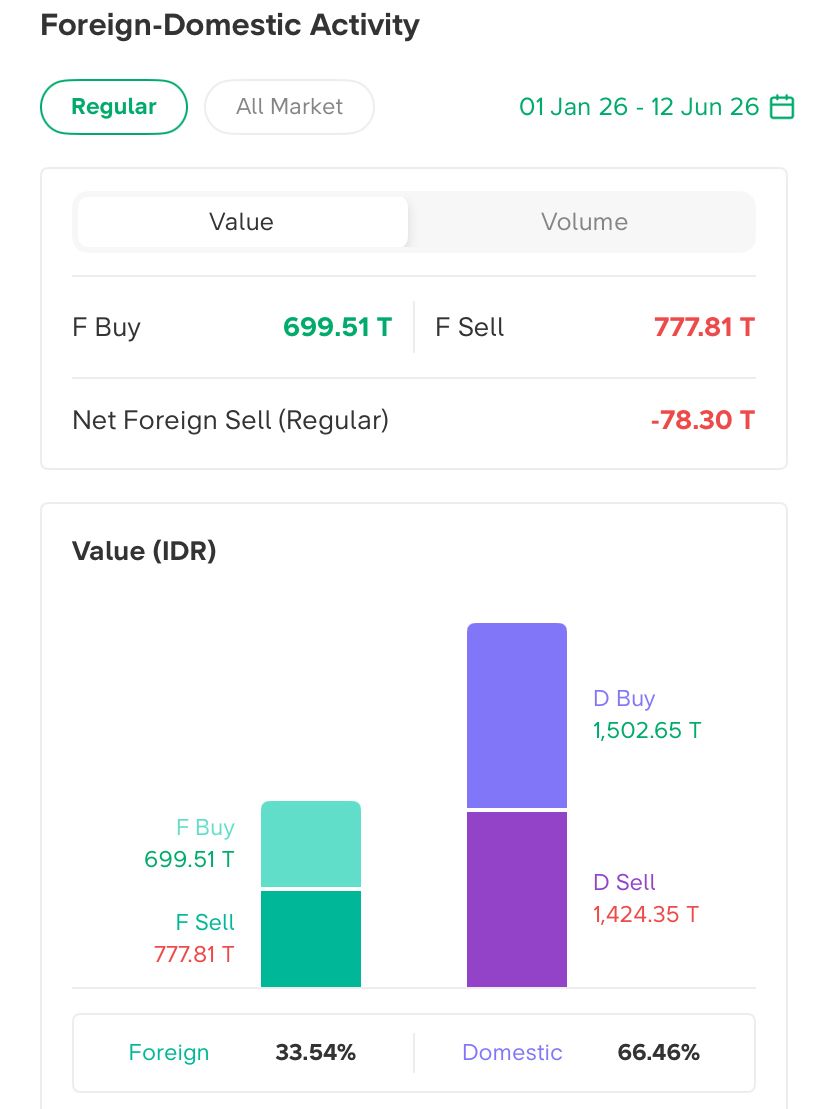

The JCI remains in a consolidation phase following its sharp correction over the past few months. While last week's 7.4% rebound was encouraging, foreign outflows persist, with net foreign selling reaching Rp78.3 trillion YTD. Looking ahead, investors will closely monitor MSCI's market accessibility review in June and S&P's outlook assessment in July as key market catalysts.

Amid this volatility, we continue to favor fundamentally strong companies that have experienced excessive sell-offs. BREN, BRPT, and CUAN appear increasingly oversold, while BRPT delivered record earnings in 1Q26. We also maintain a positive view on TPIA, supported by its transformation into a regional petrochemical consolidator and its still-attractive valuation.