On June 3, Moody’s assigned its first-ever rating to PT Danantara Investment Management (DIM) at Baa2/Negative, in line with Indonesia’s sovereign rating. The rating reinforces Danantara’s position as a government-linked entity with strong state support and improved access to global funding markets. At the same time, it highlights that Danantara’s credit profile remains closely tied to Indonesia’s sovereign credit quality, meaning any change in the sovereign rating could also influence investor perception toward Danantara.

Meanwhile, the market has been increasingly focused on speculation surrounding a potential S&P downgrade of Indonesia’s sovereign rating following its ongoing fiscal reassessment. Even so, the most realistic downside scenario remains a one-notch downgrade from BBB to BBB-, which would still keep Indonesia firmly within the investment-grade category. As a result, the risk of large-scale forced selling by global institutional investors remains limited, as most investment mandates continue to allow holdings of BBB-rated assets. The more likely impact would be pressure on the rupiah, higher government bond yields, and an increase in funding costs as investors reprice risk.

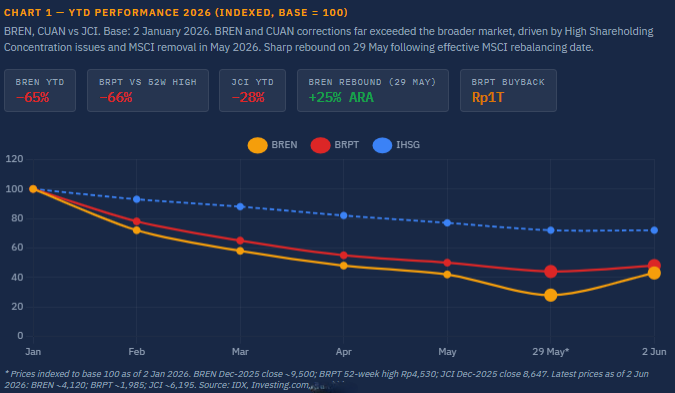

Interestingly, the JCI has already declined around 28% YTD, while foreign investors have recorded approximately IDR64 trillion of net selling this year, suggesting that a significant portion of these concerns may already be reflected in market valuations. On the macro side, Indonesia’s economic fundamentals remain relatively resilient. May 2026 inflation came in at 3.08% YoY, still within Bank Indonesia’s target range, while the Manufacturing PMI returned to expansion territory at 50.0, after previously contracting at 49.1. This suggests that the recent market weakness has been driven more by sentiment and risk perception than by a meaningful deterioration in economic fundamentals.

Against this backdrop, we believe BREN and BRPT are two names worth keeping on investors’ radar. Both stocks have seen significant corrections this year despite resilient fundamentals. BREN continues to benefit from its geothermal expansion strategy, while BRPT recently posted record earnings and announced a Rp1 trillion buyback program, signaling confidence in its long-term prospects. As technical headwinds gradually fade, market focus could increasingly shift back toward business execution and earnings growth.