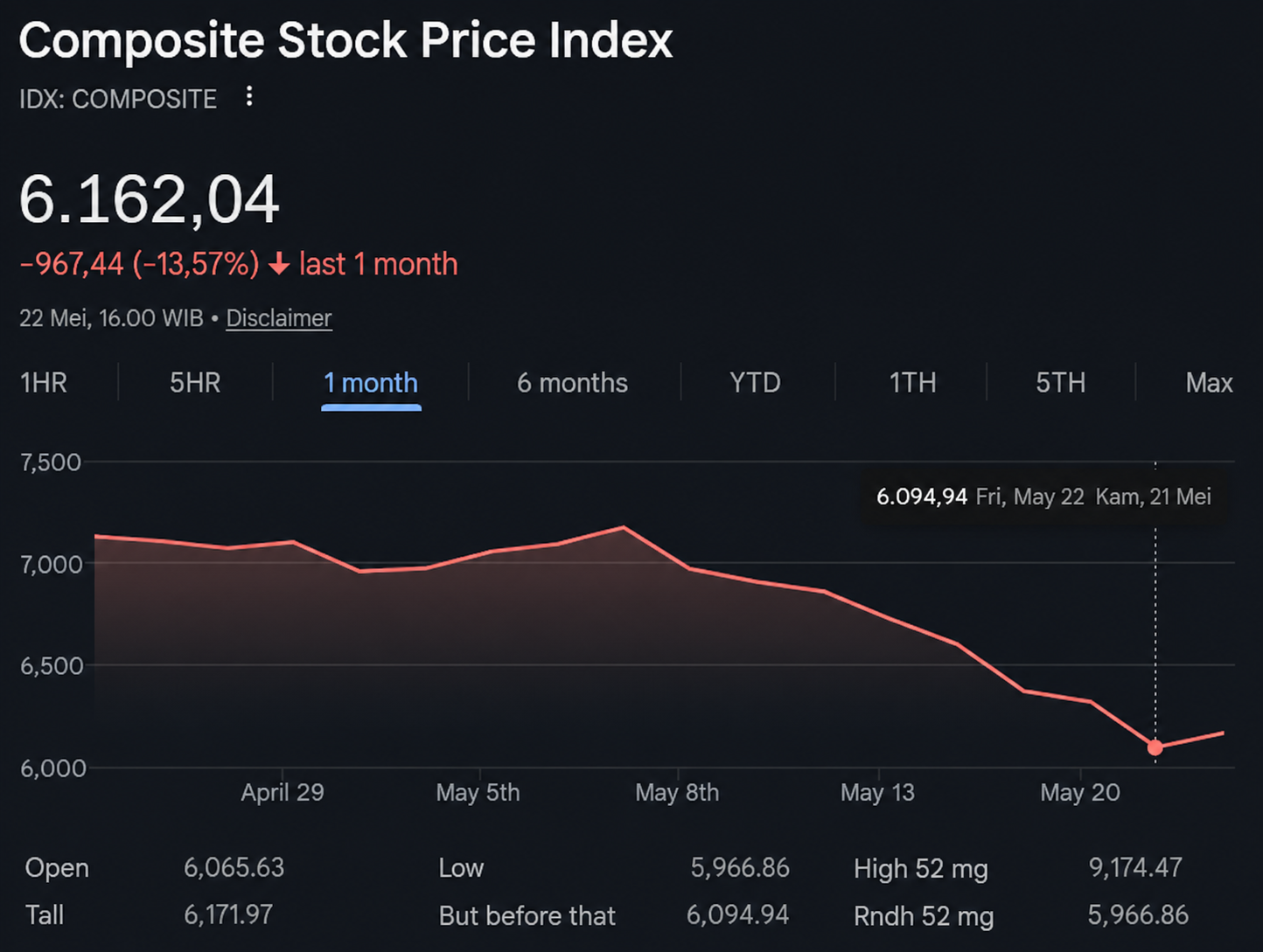

Last week was challenging for Indonesian equities as the JCI fell, making it the weakest performer among emerging Asian markets that day. Selling pressure was driven by foreign outflows ahead of the May 2026 MSCI rebalancing, particularly in DSSA, BREN, and TPIA, alongside continued weakness in the rupiah. Still, Friday’s session offered an early sign of stabilisation, with the JCI rebounding from an intraday low of 5,966 to close session one at 6,113, indicating bargain hunters have started re-entering the market.

Amid the market turbulence, the government moved to finalise two major structural policies that have been in the pipeline for some time. The first is the 100% repatriation of export foreign exchange proceeds (DHE), mandatory from 1 June 2026, requiring all commodity export earnings to be held domestically, primarily at state owned Himbara banks. Exporters are incentivised with income tax rates as low as 0% depending on how long they keep funds onshore.

The second is the mandatory channelling of exports in three strategic commodities, namely CPO, coal, and ferro alloy, through a single state owned entity, PT Danantara Sumber Daya Indonesia (DSI). Together, the two policies are projected to add approximately USD 60.9 billion in annual foreign exchange inflows.

The monopoly risk surrounding DSI remains a key market concern, although the government has emphasised tighter oversight by placing officials from the Ministry of Finance and other institutions directly within the entity to minimise potential market distortions.

For now, DSI will only record and monitor transactions through December 2026, while exporters continue trading directly with buyers. The transition toward DSI becoming an active trader is expected to begin in January 2027.

Looking ahead, markets will closely monitor whether the JCI can stabilise around the 6,000 to 6,100 range following the MSCI rebalancing, alongside how commodity linked stocks react as the DSI mechanism becomes clearer, particularly among exporters exposed to CPO and coal.

Meanwhile, the banking sector may continue offering relative defensiveness amid ongoing volatility. Banking valuations have compressed significantly in recent months, while dividend yields among several state owned banks remain attractive, supporting interest in names such as BBCA, BBRI, and BMRI.