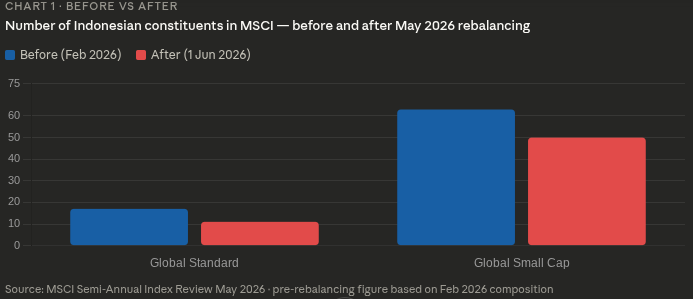

Indonesia’s domestic equity market has just absorbed a significant shock after MSCI officially released its semi-annual index review earlier this month. Six major companies were removed from the MSCI Global Standard Index, namely AMMN, BREN, TPIA, DSSA, CUAN, and AMRT, alongside thirteen additional names excluded from the Global Small Cap Index, including ANTM, BSDE, MIKA, and AALI. However, the key narrative behind this reshuffle is not deteriorating corporate fundamentals. Instead, the changes were largely driven by a technical adjustment following increased ownership transparency from Indonesian regulators, which revealed that public free float ownership in several issuers was far more concentrated than previously reflected.

The disclosure immediately triggered an aggressive market reaction, briefly dragging the Jakarta Composite Index (JCI) down to the 6,755 level on the announcement day. Market attention is now heavily focused on the potential for foreign outflows, which are projected to reach tens of trillions of Rupiah as global fund managers begin restructuring their portfolios. With the changes set to become effective on May 29th, 2026, volatility is likely to continue hovering over the market in the near term. Much of this selling pressure had already been partially anticipated since the beginning of the year, but maintaining a high level of caution remains essential.

Amid the turbulence, one encouraging development is that Indonesia’s capital market has successfully avoided the risk of being downgraded to frontier market status. The regulator’s firm steps to tighten minimum free float requirements and improve ownership transparency should be viewed as a temporary adjustment toward achieving longer-term structural progress. Global investors are now awaiting the follow-up evaluation in June, which could become a key determinant of future foreign investment sentiment toward Indonesia.

Given these dynamics, the correction heading into late May may actually present an attractive window of opportunity to accumulate quality names. Companies removed purely due to technical free float issues still maintain solid business fundamentals and deserve closer attention once market volatility stabilizes. The most rational strategy for now is to avoid impulsive buying decisions around the implementation date when liquidity conditions may become thinner. Patience remains key, while investor focus should gradually shift toward resilient names still firmly positioned within the MSCI Standard Index, such as BBCA and BMRI, which could naturally benefit from larger weighting allocations in global portfolios.