08 August 2025

Stronger Q2 Data Signals Potential Shifts in Market Focus

Market Commentary

0 comments

Last Week, we noted that Indonesia’s Q2 GDP came in stronger than expected. Rather than just revisiting the drivers, let’s look at what the numbers are signalling beneath the surface to get a more complete picture.

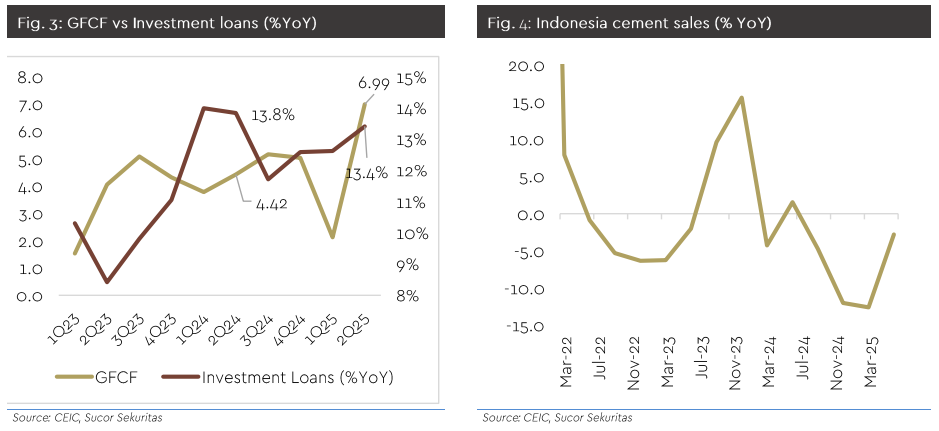

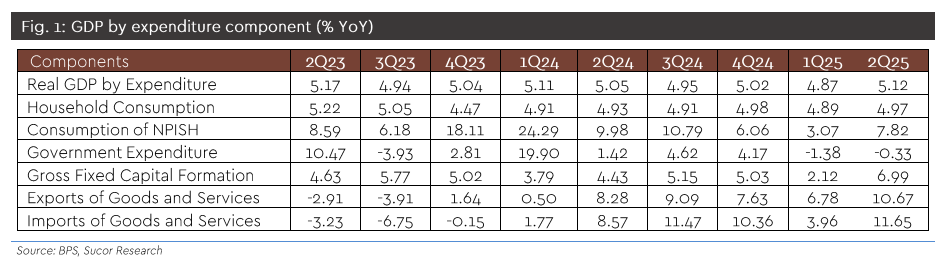

The biggest push came from gross fixed capital formation (GFCF), which jumped 6.99% YoY from just 1.21% in Q1. Most of it came from buildings and construction. In theory, this should have cement factories scrambling to keep up with orders and banks flooded with investment loan requests. In reality, cement sales were flat and investment loan growth actually slowed. It feels like a sold-out concert where the venue still has empty seats.

Then there is FDI, which fell for the first time since 2020. Exports had a solid quarter, but imports grew even faster, quietly eroding net trade contribution. The spike in machinery and equipment imports was mostly tied to projects with limited spillover into household demand, which has been stuck below 5% growth for seven straight quarters.

For the market, this matters. If the investment surge was simply a one-off from front-loaded government projects, Q3 growth could slip toward 4.9% before a mild recovery in 2026. That would leave equities leaning more on policy support than on pure economic momentum.

The good news is that BI has already begun easing by trimming SRBI, with potential rate cuts that could bring the 10-year yield down to around 5.8%. This is a sweet spot for rate-sensitive sectors such as property, construction, and financing, as well as yield proxies like high-dividend plays.

In essence, the Q2 headline may be loud, but the fine print is quieter. For investors, the smarter move is to position in sectors that benefit from liquidity rather than relying solely on GDP momentum.

The biggest push came from gross fixed capital formation (GFCF), which jumped 6.99% YoY from just 1.21% in Q1. Most of it came from buildings and construction. In theory, this should have cement factories scrambling to keep up with orders and banks flooded with investment loan requests. In reality, cement sales were flat and investment loan growth actually slowed. It feels like a sold-out concert where the venue still has empty seats.

Then there is FDI, which fell for the first time since 2020. Exports had a solid quarter, but imports grew even faster, quietly eroding net trade contribution. The spike in machinery and equipment imports was mostly tied to projects with limited spillover into household demand, which has been stuck below 5% growth for seven straight quarters.

For the market, this matters. If the investment surge was simply a one-off from front-loaded government projects, Q3 growth could slip toward 4.9% before a mild recovery in 2026. That would leave equities leaning more on policy support than on pure economic momentum.

The good news is that BI has already begun easing by trimming SRBI, with potential rate cuts that could bring the 10-year yield down to around 5.8%. This is a sweet spot for rate-sensitive sectors such as property, construction, and financing, as well as yield proxies like high-dividend plays.

In essence, the Q2 headline may be loud, but the fine print is quieter. For investors, the smarter move is to position in sectors that benefit from liquidity rather than relying solely on GDP momentum.

Written by Boris, the Broker

Comments