28 October 2024

A New Champion Emerges

Market Commentary

0 comments

Right now, the global financial market is facing the possibility of rising bond yields, not because of fears of an economic downturn, but due to growing concerns about geopolitical conflicts.

Even though the Federal Reserve is expected to lower interest rates to 3.5% by the end of 2025, bond yields could still spike as traders brace for risks, especially from tensions in the Middle East.

If a conflict does occur, it could lead to a significant rise in oil prices, which in turn, might push global inflation even higher.

In such a scenario, companies with large exposure to oil production stand to gain. One company that is well-positioned to take advantage of this opportunity is ENRG.

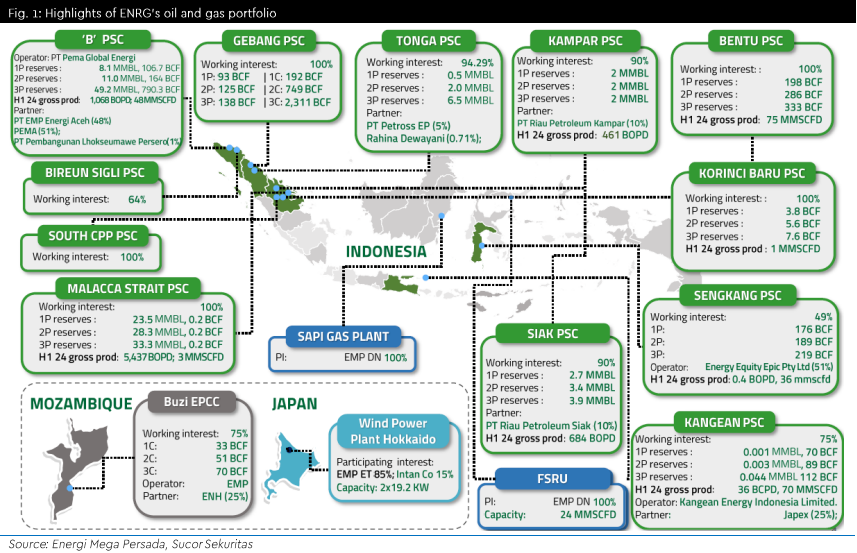

As a major player in Indonesia's oil and gas industry, ENRG is currently producing around 7,686 BOPD and 232mn cubic feet of gas daily. When combined, this is equivalent to about 46,332 BOPD.

This makes the company a significant force in the sector.

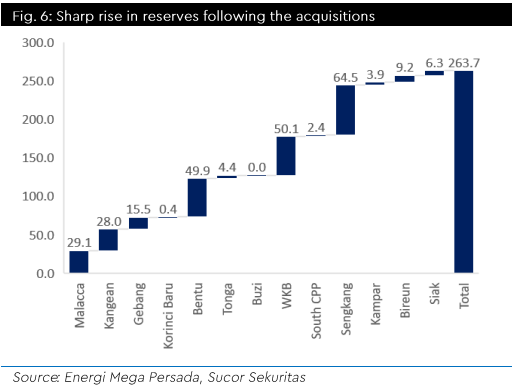

In recent years, ENRG hasn’t just been sitting still, they’ve been aggressively expanding. They’ve not only increased their stake in existing blocks but also acquired new assets across Indonesia.

For example, between 2020 and 2022, they took over Malacca Strait Block, Kangean, South CPP, and Sengkang Block.

Then in 2024, they successfully acquired 90% ownership in both Siak and Kampar blocks.

Even though the Federal Reserve is expected to lower interest rates to 3.5% by the end of 2025, bond yields could still spike as traders brace for risks, especially from tensions in the Middle East.

If a conflict does occur, it could lead to a significant rise in oil prices, which in turn, might push global inflation even higher.

In such a scenario, companies with large exposure to oil production stand to gain. One company that is well-positioned to take advantage of this opportunity is ENRG.

As a major player in Indonesia's oil and gas industry, ENRG is currently producing around 7,686 BOPD and 232mn cubic feet of gas daily. When combined, this is equivalent to about 46,332 BOPD.

This makes the company a significant force in the sector.

In recent years, ENRG hasn’t just been sitting still, they’ve been aggressively expanding. They’ve not only increased their stake in existing blocks but also acquired new assets across Indonesia.

For example, between 2020 and 2022, they took over Malacca Strait Block, Kangean, South CPP, and Sengkang Block.

Then in 2024, they successfully acquired 90% ownership in both Siak and Kampar blocks.

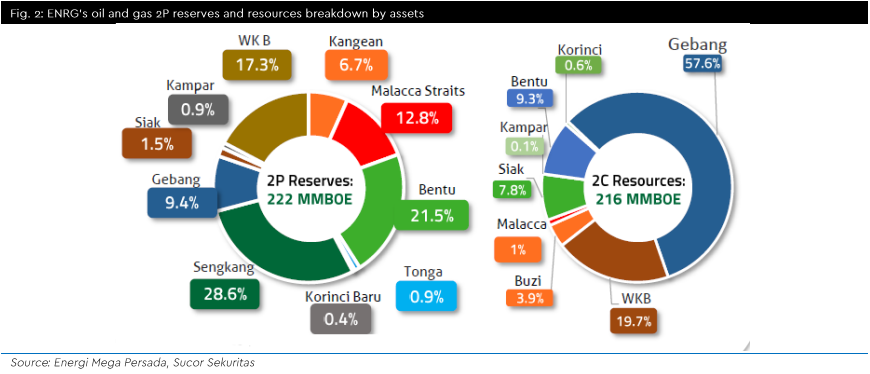

One of ENRG’s biggest “treasures” is Sengkang Block in South Sulawesi. This block is their key asset, especially when it comes to gas production and reserves.

Sengkang holds 28.6% of ENRG’s total 2P reserves.

Recently, they managed to fully take control of the block by acquiring the remaining 51% ownership.

The goal? To give them more flexibility in managing the block’s development and maximizing gas production there.

Bentu Block in Riau is ENRG’s second-largest gas producer.

This block contributes around 27% of ENRG’s total oil and gas production. Its 2P reserves are also significant, making up 21.5% of ENRG’s total 2P reserves.

What’s interesting is that ENRG owns 100% of both these major blocks, Sengkang and Bentu, meaning they have full control over these highly profitable assets.

As for the contracts, they’re secure, with Sengkang running until 2042 and Bentu until 2041.

Apart from gas, ENRG also has a strong presence in the oil sector.

Malacca Block is one of their main oil assets, contributing about 13% of their total oil production in 1H24.

And they’re not stopping there. ENRG recently acquired two more oil blocks, Siak and Kampar in Riau.

These two blocks combined produced 1,145 BOPD in 1H24. What’s exciting is that they’re optimistic this number will jump to 3,000 barrels/day by 2026.

Sengkang holds 28.6% of ENRG’s total 2P reserves.

Recently, they managed to fully take control of the block by acquiring the remaining 51% ownership.

The goal? To give them more flexibility in managing the block’s development and maximizing gas production there.

Bentu Block in Riau is ENRG’s second-largest gas producer.

This block contributes around 27% of ENRG’s total oil and gas production. Its 2P reserves are also significant, making up 21.5% of ENRG’s total 2P reserves.

What’s interesting is that ENRG owns 100% of both these major blocks, Sengkang and Bentu, meaning they have full control over these highly profitable assets.

As for the contracts, they’re secure, with Sengkang running until 2042 and Bentu until 2041.

Apart from gas, ENRG also has a strong presence in the oil sector.

Malacca Block is one of their main oil assets, contributing about 13% of their total oil production in 1H24.

And they’re not stopping there. ENRG recently acquired two more oil blocks, Siak and Kampar in Riau.

These two blocks combined produced 1,145 BOPD in 1H24. What’s exciting is that they’re optimistic this number will jump to 3,000 barrels/day by 2026.

ENRG isn’t just focusing on upstream activities like exploration and production anymore, they’ve also started expanding into the downstream sector.

One of their big moves was acquiring Floating Storage Regasification Units, such as Sulawesi Regas Satu in 2023 and Gandini in 2024.

These floating units for storage and regasification give ENRG more capacity in the gas supply chain, especially to meet domestic energy needs.

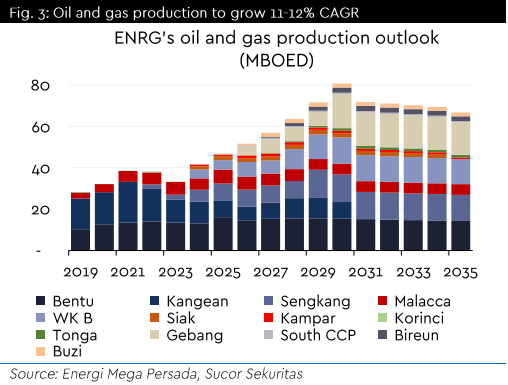

This aggressive expansion strategy is starting to pay off. Their oil and gas production has already seen a sharp increase in 2024.

The projection is that ENRG’s total production will reach 81,000 BOEPD by 2030, assuming no further acquisitions.

One of their big moves was acquiring Floating Storage Regasification Units, such as Sulawesi Regas Satu in 2023 and Gandini in 2024.

These floating units for storage and regasification give ENRG more capacity in the gas supply chain, especially to meet domestic energy needs.

This aggressive expansion strategy is starting to pay off. Their oil and gas production has already seen a sharp increase in 2024.

The projection is that ENRG’s total production will reach 81,000 BOEPD by 2030, assuming no further acquisitions.

The main drivers behind this production surge are WK B Block and Gebang Block, which will be their key assets moving forward.

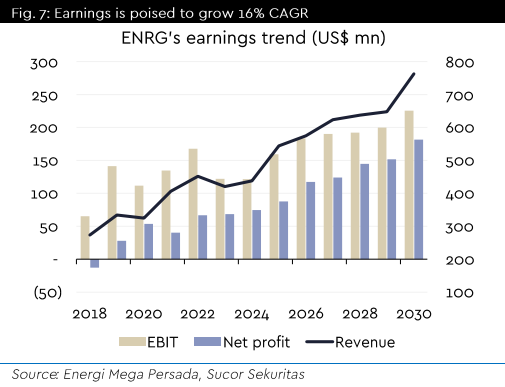

On the financial side, this projected production growth will have a big impact.

Using conservative oil price assumptions, between USD 70 to USD 78/barrel, and gas prices ranging from USD 6.5 to USD 7.5/mmbtu, ENRG’s revenue is expected to grow at a CAGR of 11% over the next three years.

Additionally, ENRG has secured financing from Bank Mandiri at an interest rate of 8-9%, a significant improvement compared to their previous foreign financing, which had rates as high as 30%.

This shift in financing terms will greatly enhance ENRG’s cost efficiency and profitability going forward.

As for net profit, ENRG is predicted to grow even faster. They’re estimating a CAGR of 19% through 2026.

On the financial side, this projected production growth will have a big impact.

Using conservative oil price assumptions, between USD 70 to USD 78/barrel, and gas prices ranging from USD 6.5 to USD 7.5/mmbtu, ENRG’s revenue is expected to grow at a CAGR of 11% over the next three years.

Additionally, ENRG has secured financing from Bank Mandiri at an interest rate of 8-9%, a significant improvement compared to their previous foreign financing, which had rates as high as 30%.

This shift in financing terms will greatly enhance ENRG’s cost efficiency and profitability going forward.

As for net profit, ENRG is predicted to grow even faster. They’re estimating a CAGR of 19% through 2026.

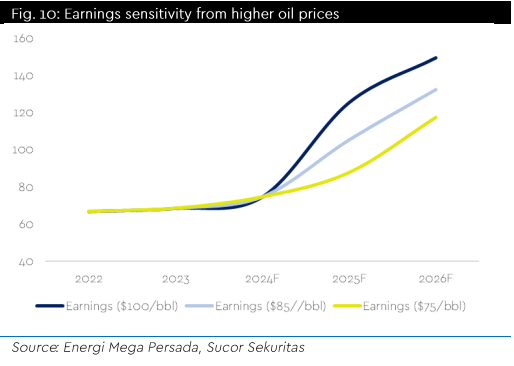

Even though we’ve set a conservative oil price forecast between USD 70 and USD 78/barrel, we can’t ignore the possibility of oil prices spiking.

We project that if oil prices surge to USD 100/barrel, ENRG’s net profit in 2025 could reach USD 125 mn.

We project that if oil prices surge to USD 100/barrel, ENRG’s net profit in 2025 could reach USD 125 mn.

This figure represents a 28% increase from our base projection and an impressive 65% jump compared to the estimated net profit for 2024.

So, if oil prices do rise, the impact on ENRG will be massive.

We’re initiating coverage on ENRG with a BUY recommendation and setting a target price of IDR 720.

It’s important to note that our valuation does not yet factor in cash flows from non-operational assets like Bireun, Gebang, South CPP, and Buzi, which are projected to start operating in 2026.

These assets were acquired at a total cost of USD 225 mn and are expected to contribute significantly in the future.

Why do we prefer ENRG?

Because with ENRG, we can calculate the valuation of each block in detail.

Unlike MEDC, ENRG is completely open, with all the numbers clearly laid out, and we already have the data.

So, if oil prices do rise, the impact on ENRG will be massive.

We’re initiating coverage on ENRG with a BUY recommendation and setting a target price of IDR 720.

It’s important to note that our valuation does not yet factor in cash flows from non-operational assets like Bireun, Gebang, South CPP, and Buzi, which are projected to start operating in 2026.

These assets were acquired at a total cost of USD 225 mn and are expected to contribute significantly in the future.

Why do we prefer ENRG?

Because with ENRG, we can calculate the valuation of each block in detail.

Unlike MEDC, ENRG is completely open, with all the numbers clearly laid out, and we already have the data.

This makes us feel more confident in bringing clients onboard, as we can value this company with much more detail.

As we all know, valuing an oil and gas company isn’t an easy task. There are many factors to consider, from oil and gas reserves, operating costs, to commodity price fluctuations.

With ENRG, the transparency of their data makes it easier for us to calculate the valuation accurately, block by block.

This allows us to provide clearer and more solid projections for you.

As we all know, valuing an oil and gas company isn’t an easy task. There are many factors to consider, from oil and gas reserves, operating costs, to commodity price fluctuations.

With ENRG, the transparency of their data makes it easier for us to calculate the valuation accurately, block by block.

This allows us to provide clearer and more solid projections for you.

Written by Boris, the Broker

Comments