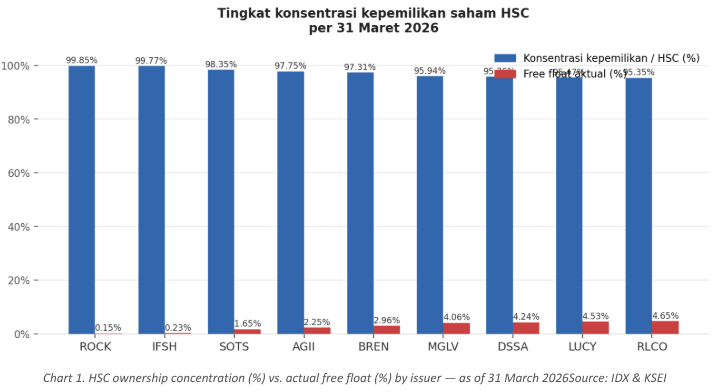

April 2, 2026, on the last trading day before the Good Friday holiday on April 3, quietly marked a new milestone in Indonesian capital market reform. The Indonesia Stock Exchange (IDX), together with KSEI, officially released the first-ever list of issuers with high shareholding concentration (HSC), as part of a broader push to strengthen investor confidence in the domestic market. Based on data as of March 31, 2026, nine issuers were flagged, with ownership concentration ranging from 95% to nearly 100% of total shares outstanding, with BREN and DSSA, both constituents of the MSCI Indonesia index, drawing the most attention given their sizable market capitalizations of IDR 642 trillion and IDR 542 trillion respectively.

.png)

The key is to read this with a clear head. IDX Acting President Director Jeffrey Hendrik was explicit that inclusion on the HSC list does not automatically indicate any violation of capital market rules, but rather serves as additional information for investors to make more informed decisions. The initiative is aligned with practices seen in global exchanges such as the Hong Kong Stock Exchange, and comes amid increasing scrutiny from index providers like MSCI. Importantly, the benefit of the doubt remains intact. Concentrated ownership does not inherently imply manipulation, and in many cases reflects the historical structure of Asian conglomerates that have not widely distributed public float. This view is also echoed by analysts at Indopremier and MNC Sekuritas, who frame the HSC list as an early warning mechanism rather than an accusation.

That said, the near term market reaction has been tangible. BREN dropped as much as 12.73% following the release, highlighting investor sensitivity to potential index eligibility risks. If a Hong Kong style framework were to be adopted by MSCI, both BREN and DSSA could face index exclusion and a minimum 12 month reinclusion delay, while also being ineligible for new inclusion until achieving at least a 15% free float, a scenario that raises the risk of forced selling by passive global funds tracking MSCI benchmarks.

.png)

Looking ahead, markets will be closely watching two key catalysts. The FTSE Russell interim review on April 7, 2026 will determine whether Indonesia maintains its Emerging Market status, and the MSCI index review on May 12, 2026 remains the primary driver of global fund flows. OJK has signaled active engagement with index providers to ensure alignment with international standards. For now, maintaining a measured and neutral stance appears prudent as the regulatory dialogue unfolds, recognizing that while this reform is structurally positive over the long term, it may continue to drive technical volatility in HSC linked names in the near term.