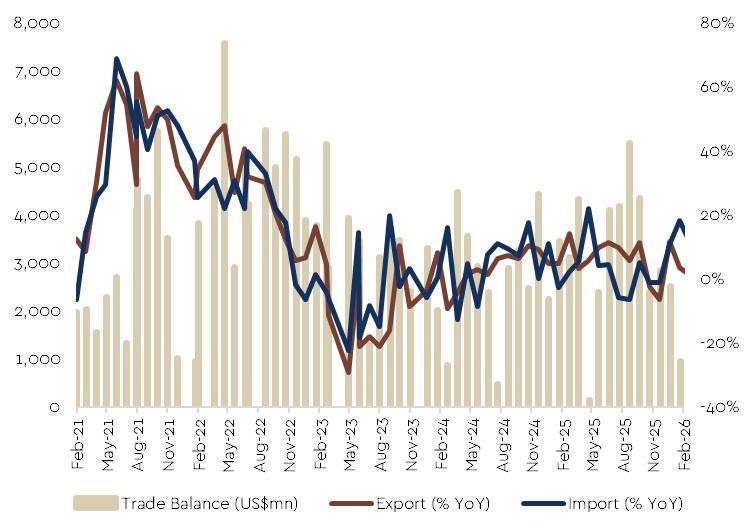

Indonesia just recorded its 69th consecutive month of trade surplus in February. While the US$1.28 billion figure came in slightly below market expectations, there is a compelling detail beneath the surface: capital goods imports saw double-digit growth. This is a clear signal that investment activity on the ground is gaining serious traction. Rather than viewing this as a sign of weakness, our economist sees it as a transition phase before we enter a significantly stronger quarter.

Looking ahead to March, the surplus is expected to widen substantially toward US$2.4 billion, driven by naturally slower import activity during the Lebaran holiday season. Simultaneously, the rise in global oil prices due to geopolitical tensions is predicted to trigger a rally in key commodities like coal and nickel. If this scenario unfolds, it will provide a buffer for the Rupiah, keeping it steady around the Rp16,800/USD range, and create room for 10-year SBN yields to drop toward 6.70% in April,offering a strategic entry point for fixed-income investors.

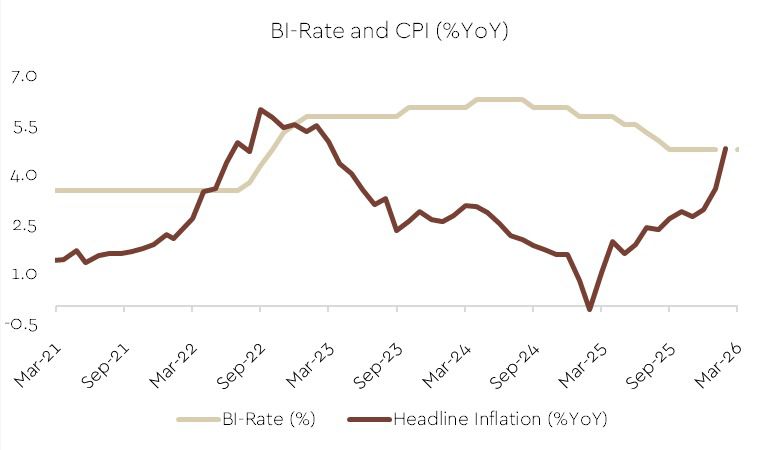

On the inflation front, the March reading of 3.48% was relatively tame and landed below initial projections. However, challenges remain, particularly regarding potential adjustments to non-subsidized fuel prices to maintain fiscal health. Should global oil prices remain elevated, the market should anticipate a possible cumulative interest rate hike of up to 100 bps over the next year. While this dynamic may seem challenging, historically, a negative real interest rate environment has often provided a supportive foundation for the equity market.

Overall, the market impact remains constructive due to solid domestic fundamentals. With the PMI remaining expansionary, GDP growth for 1Q26 is projected to be the strongest in three years. As long as the real sector continues to gain momentum, the stock market has a strong fundamental reason to stay in the green. In short, while the Indonesian macro landscape is currently complex, the trajectory remains firmly on an upward path.