26 May 2025

Soft Start, Strong Finish Ahead

Market Commentary

0 comments

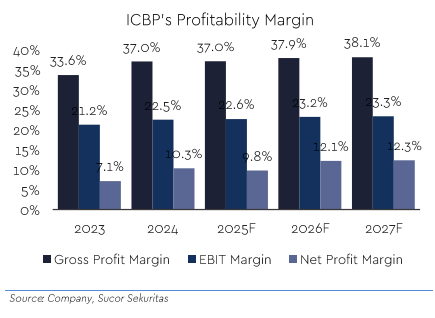

ICBP is set for a promising year ahead, supported by falling raw material costs and upcoming price adjustments that should lift margins in the coming quarters. With CPO prices down 13% ytd and wheat prices stable, the company is expected to recover its gross margin to around 38% by the end of 2025.

A planned 3% increase in average selling prices in the second half of the year should further strengthen profitability. Backed by solid free cash flow, ICBP is also on track to reach a net cash position by 2028, providing more flexibility for dividends, potential acquisitions, and reducing volatility to forex risk from its USD-denominated bonds.

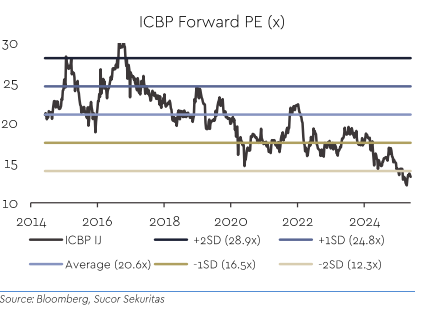

Despite a soft start in 1Q25—where the company posted just 2% YoY sales growth and saw margin contraction due to delayed pricing—the fundamentals remain intact. Core profit is projected to grow 8.2% in 2025 and 6.5% in 2026. Currently trading at only 12.1x forward PE, well below its 10-year average, ICBP offers an attractive valuation for long-term investors. We maintain our BUY call with a target price of Rp13,000.

A planned 3% increase in average selling prices in the second half of the year should further strengthen profitability. Backed by solid free cash flow, ICBP is also on track to reach a net cash position by 2028, providing more flexibility for dividends, potential acquisitions, and reducing volatility to forex risk from its USD-denominated bonds.

Despite a soft start in 1Q25—where the company posted just 2% YoY sales growth and saw margin contraction due to delayed pricing—the fundamentals remain intact. Core profit is projected to grow 8.2% in 2025 and 6.5% in 2026. Currently trading at only 12.1x forward PE, well below its 10-year average, ICBP offers an attractive valuation for long-term investors. We maintain our BUY call with a target price of Rp13,000.

Written by Boris, the Broker

Comments